REsourcEU: Baseless?; Nigerian Princes & Rare Earth; Rare Earth Smuggle; Eudialyte remains a Dud; Utah RE in Halloysite & Illite; and the lot.

Rare Earth 14 December 2025 #190

Note

A proven rare earth non-resource is to go to Transylvania hoping to become separated rare earths, at a place near to what is known as Count Dracula’s Castle. This happening would be about as miraculous as the vampire himself rising from his coffin. Read in the “Companies” section below what the real purpose of this futile exercise could be.

Other companies featured today are Ucore, ReAlloys, Quadrant/Zhijian Holdings, Viridis, Meteoric, Chilwa, Arnold Magnetics, Namibia Critical Metals, ASM, VAC, Leading Edge Materials, Rainbow, Pensana, Brazilian Rare Earths, ReAlloys, Ramaco, Ionic MT, Tronox, Barkly, ABx and - with a fair amount of pity, sprinkled with disgust - USA Rare Earths.

We discuss the rare earths in halloysite and most probably illite in Utah, USA.

Responding to accusations of negativism we reveal what we think might work in rare earths.

China rare earth smuggle

There are documented cases of both, import smuggle and export smuggle.

One case dates back to 2017, closed in 2024, which involves the import and massive under-declaration of the value of mixed rare earth carbonate from Myanmar. Since the formation of China Rare Earth Group this particular avenue of pleasure should have been closed anyway.

Another case is the export smuggle of rare earths from China to India via Mongolia:

For example, high-purity dysprosium and terbium are directly mixed into soldering materials and exported as ferroalloys, circumventing the control list. This is not a small-scale operation; it’s large-scale enough to affect global supply. The smuggling chain doesn’t stop at exports but extends to the transit stage. Goods are sent to places like India via express parcels, where companies resell them to Western buyers, earning huge profits per ton.

India plays a significant role in the supply chain. Reports indicate that some Indian companies purchase goods from smuggling networks at prices 60% higher than market value and then resell them at inflated prices. Thailand and Mexico have also served as popular transit points, but Chinese customs began monitoring them in June 2025, exploiting technical loopholes to sever the core routes.

Those foreign companies were directly added to the unreliable entity list, effectively cutting them off from rare earth business with China. This demonstrates the government’s determination to upgrade regulations. In June, the government launched a rare earth tracking system, recording the customer, quantity, and destination of each shipment on the platform, effectively closing loopholes in the system. Foreign companies have attempted to build alternative supply chains in Thailand and Mexico, but these projects have repeatedly failed due to technological bottlenecks.

On July 19, this office publicly announced the launch of a crackdown on the smuggling of key minerals, coordinating resources from multiple departments. To date, the operation has resulted in the criminal detention of 43 people and the halving of export quotas for 37 violating companies. 32,000 sensors have been deployed along the China-Mongolia border, using vibration frequencies to identify ore in freight cars, achieving a detection rate as high as 98%.

And:

Three Indian companies have been permanently banned from purchasing rare earth elements from China, and Tata Group’s inventory was once only enough for three days, causing severe hardship for Indian manufacturers. This is reaping what they sow; compliant channels were readily available, but they chose to steal, ultimately blocking their own path.

as well as:

China has a clear advantage in rare earths, but foreign countries don’t lack minerals; what they lack is refining technology. The government has required companies to report information on core technical personnel and establish a talent database to prevent technology leaks. This isn’t just empty talk; the action itself has addressed the issue of internal coordination. Public participation is crucial; the public must be wary of the lure of high profits and avoid losing more than they gain. The official announcement serves two purposes: first, to remind everyone to safeguard resource security, and second, to warn foreign forces. The special operation continues, with border sensors and tracking systems working in tandem, effectively dismantling the smuggling chain.

And their passports have been taken….

This here is particularly serious:

Some domestic companies, unable to resist the high profits, have become internal traitors, helping to forge labels and erase traces.

Being accused of violating rare earth “national security” can result stiff penalties. And, rest assured, thereafter you will find no more happiness in life.

Look at the rare earths under dual-use license since 4 April 2025 and their domestic prices:

Terbium oxide, US$900/kg

Dysprosium oxide, US$200/kg

Yttrium oxide, US$8.50/kg

Gadolinium oxide, US$23/kg

Samarium oxide, US$2.35/kg

Lutetium oxide, US$730/kg

Scandium oxide, US$700/kg

Are 60% higher prices worth the risk? We have sincere doubts.

Generally the air gets pretty thin for unregulated trade operation in whatever product in China:

The New 2025 China Import-Export Regulations: What’s Changed – And What You Should Do Now

In October 2025, China enacted a comprehensive tightening of its export and customs regime. The new regulation requires that every exporter and importer operating in China be officially registered and identifiable to the tax and customs authorities. It also requires an Import or Export license and the relevant business scope.

In practical terms, this means the end of the old “grey-trade” model in which intermediary so- called “trading companies” exported goods under their own license – without revealing the real manufacturer. That model may have been convenient (and cheap), but it exposed exporters and importers to serious risks.

The new regulations are officially dealing with Exports, but our on-the-ground experience shows that the tightening is an overall scheme applied to Imports, too [i.e. has the foreign rare earth raw material supplier a process license from China?].

As of October 1, 2025:

All export-related documentation – invoices, statements, export declarations – must clearly reflect the actual source of the goods and identify the real manufacturer.

Brokerage/trading firms are no longer allowed to submit export declarations on behalf of a third-party manufacturer. The exporting entity now must assume full ownership and responsibility for the goods (in more simplified words, they will actually need to buy the goods).

Failure to comply – including inconsistencies or lack of transparency in documentation – may result in delays, credit rejection (e.g. VAT refunds), or even fines.

That has interesting implications on product liability, too.

Are rare earths commodities?

Over and over again we hear from exquisite experts about rare earth commodities. We disagree to this classification.

Commodities are:

Fungible, interchangeable

Uniform, standardised products

Raw materials

Tradable on commodity exchanges

When talking about rare earths “commodities”, people actually refer to rare earth compounds such as rare earth -oxides, -chlorides, -fluorides, -carbonates, -hydroxides, -phosphates and -sulfates:

The rare earth compounds market outside China could be worth an estimated ca. US$1 bio/year.

That market consists of up to 50 different rare earth compounds of potentially up to 100 different specifications in total.

Some rare earth compounds are added directly “as-is” to applications, hence defy the definition of a raw material commodity.

There are no industrial standards for rare earth products in the West. Only in China. There are 15 international ISO rare-earth-related standards in the West. These are about vocabulary, packaging, recycling, sustainability and determination of some quality parameters. Since 2014 the ISO working group in charge of rare earths has not published one single industrial standard for a rare earth product.

As to the international market of these “commodities”:

China exports rare earth compounds to dozens of countries. But regularly Japan is between 40-50% of the entire rare earth compounds export value from China.

If you look at the smaller market of rare earth metals and alloys, then Japan is typically north of 60% of the entire export volume from China.

Some like to refer to NdPr oxide being a commodity:

NdPr oxide is the non-separated form of combined neodymium and praseodymium as it is found in nature.

The proportion of Nd and Pr to one-another is different from one rare earth deposit/mine to another, anywhere between 70:30 and 85:15.

The published price of NdPr oxide in China is a mathematically adjusted price, reflecting an idealised Nd to Pr ratio of 75:25.

In fact, downstream from NdPr oxide separated, pure neodymium or pure praseodymium, as the case may be, need to be added in order to create the proportion deemed ideal for magnet production.

It is not NdPr oxide that is used for producing NdFeB magnets, it is NdPr metal, or rather an alloy, if you will, a different product altogether.

A former CEO of a western rare earth company defines rare earths as specialty chemicals. We agree.

Misrepresentations

Some rare earth hopefuls go a long way in order to spin stories that often are pretty far removed from fact. Some tell outright lies. They do so, because their “assets” are often of no merit at even 2040 forecast prices. They pin hope to extend their certain expiry on investors’ as well as governments’ naïvity, who often do not (want to?) notice the yawning gap between fairytales and reality.

Related to such spins certain junior miners seem to hope that the results of programmes like EURARE have been forgotten.

Bad news for them: the results have not been forgotten. They have been meticulously preserved. A big thank you to one of our most senior, highly valued contributors.

See below in the “Companies” section.

Nigerian rare earth hype

Time and time again rare-earth-virgins in the Western media and some rare-earth infotainment upstarts fall for a rare earth spin.

This time it is Nigeria, which is notorious for its princes wanting to hand over fortunes to complete strangers for a “fee”.

Back in June 2025 a Nigerian miner called Hasetins announced a rare earth separation project for US$400 mio.

This was the 9th time in four years we have heard from a Nigerian company that it wants to go downstream in monazite, separated from heavy mineral sands.

Actually, in our view, Hasetins’ project is about increasing the current HMS separation capacity from 6,000 t/y to 18,000 t/y. That requires an investment for gravitational separation in the hundred thousands of dollars, equivalent to hundreds of millions of Nigerian Naira.

Concretely, we are under the strong impression that the amount should be 400 million Nigerian Naira (US$275,000), not US Dollars and it is a heavy mineral sands (HMS) separation, not a rare earth separation.

Hasetins are currently asking everyone & sundry to buy more monazite, they are not asking customers to express interest in separated rare earths.

High contents of radioactive material

Monazite from Nigeria often has a particularly high content of radioactive material, 10-20 times higher than monazite from alternative African origins.

The Nigerians continuously ship monazite under the goods description of “Phosphocerite” as general cargo at cheap freight rates to China. Actually, such Nigerian monazite should be classified as International Maritime Dangerous Goods Code (IMDG) Class VII, which is under rigid restrictions and hellishly expensive to ship.

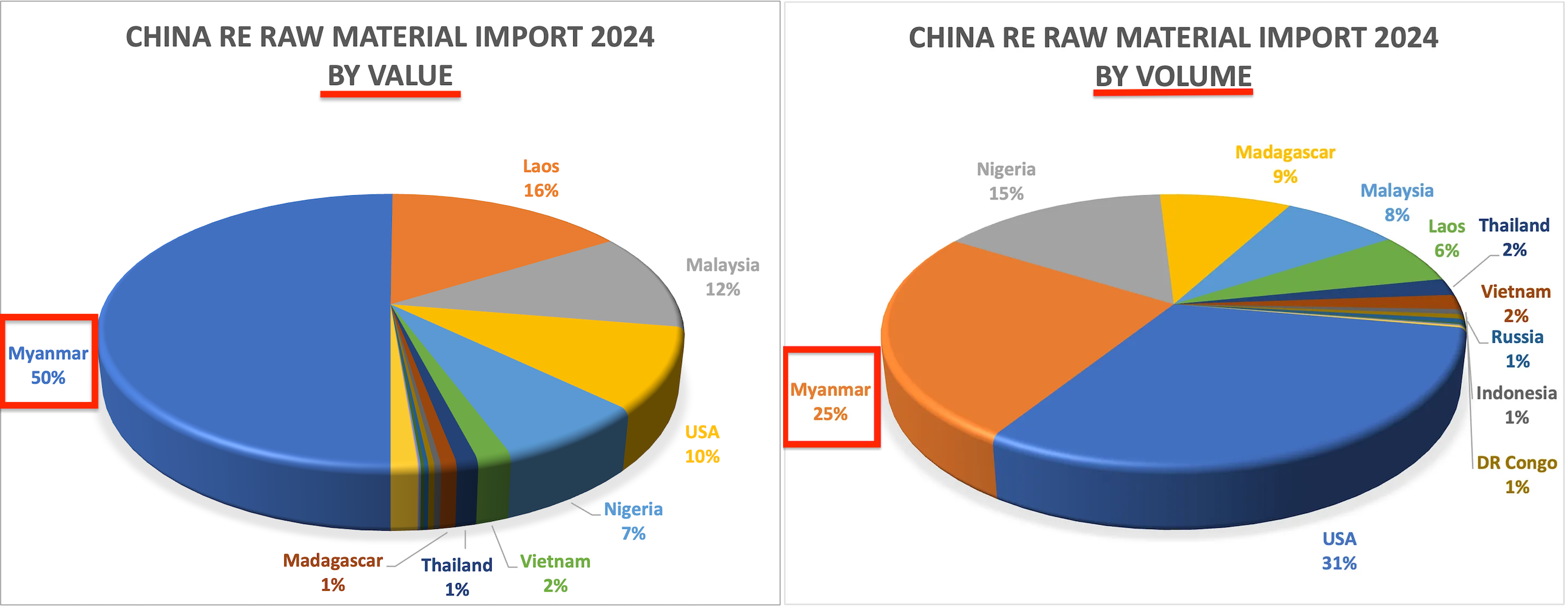

Brazil - the new Myanmar?

It is quite obvious that mining in Myanmar is creating fallout for neighbouring countries that will be more and more controversial for Beijing to ignore.

70 million people live directly from the Mekong River. Upstream tributaries of the Mekong are being massively polluted by China’s miners and their subservient local partners.

In the face of this deliberate, potentially massive environmental and economic impact, eventually wiping food and water from tables of also socialist brother countries, the pledge of China’s Prime Minister Li Qiang at the G20 to “promote the construction of an inclusive global green mining and mineral value chain“ sounds outrageously hypocritical. China’s credibility again is being challenged by itself.

China needs to do something in order to live-up to the self-created, lofty aspirations.

Since enforcing even basic environmental standards in lawless Myanmar has no prospect of success, for retaining some residual credibility China needs to replace Myanmar, particularly in rare earths. Replacing 25% of China’s rare earth import dependency by volume, being 50% by value, is no small task.

Owing to the transfer of tariff-ruined MP Materials to US-state control also the bastnaesite supply from USA has gone missing.

Potential shortage

In total China would need to replace 40% of its rare earth imports by volume and 30% of its rare earth imports by value - only to maintain the 2024 status quo. Add a rare earth growth rate of ca. 8% per year.

Option: Help from Comrades

Socialist brother countries Laos and Vietnam won’t help. Laos is an expensive mining place and Vietnam has a rare-earth-standoff with China, similar to Malaysia’s: China can’t legally provide downstream know-how abroad anymore, while Malaysia and Vietnam categorically refuse to export unprocessed rare earth raw material to China.

Option: Australia

Australia is firmly committed to the increasingly dated-looking AUKUS. In spite of the near complete absence of domestic rare earth demand, it is even ready to burn Australian tax payer money in order to solve a foreign AUKUS country’s rare earth problems. All that at enormous cost and no visible economic benefit.

In German you would call this behaviour Kadavergehorsam, loosely translated as obedience beyond death.

Australian imports of rare earth permanent magnets are even smaller than tiny Singapore’s. And it is the single most expensive mining country out there, as apparently not even nickel can be mined in Australia competitively anymore.

Option: Africa

Much of Africa’s rare earth related exports are the result of artisanal mining. In order to introduce some scale and to replace MP Materials, China’s Shenghe Resources has just acquired a rare earth asset in Tanzania for a pittance. As the recent development in Tanzania shows, there is substantial risk involved.

Option: Brazil

Brazil ticks all the boxes for China:

Member of BRICS ✅

Politically left-leaning government ✅

A dozen or so cash-strapped junior rare earth miners nursing large rare earth resources similar to Myanmar’s, plus hard-rock and heavy mineral sands options ✅

Mining-friendly infrastructure ✅

Complete China-dependence on IAC mining/processing chemicals ammonium sulphate, ammonium bicarbonate and magnesium sulphate ✅

Jeitinho Brasileiro, the Brazilian “little trick”: “a method of accomplishing a goal by circumventing or bending the rules or transgressing social conventions.” ✅

In our view Brazil may have become simply irresistible for national Chinese rare earths resource investments.

Here a write-up of a not really non-governmental propaganda agency of June this year:

With the increasing global demand for green energy and high-tech products, the prospects for cooperation between China and Brazil in the rare earth sector are broad. China’s technology and experience can help Brazil achieve breakthroughs in the development and utilisation of rare earth resources, while Brazil’s abundant mineral resources are also an important support for China’s development.

Prominent investments of CMOC Group Limited (niobium & phosphates), China Nonferrous Metal Mining Group (CNMC) (tin, niobium, tantalum) and Baiyin Nonferrous (copper) are already there. Add to that the 2011 investment under the lead of Baowu Group in the globally dominant niobium miner CBMM for a 15% shareholding.

There is a niobium MoU between China’s Xinhai Mining Technology & Equipment and rare earth hopeful St. George Mining, one of Mrs Rinehart’s rare earth bets, however, a technical report of 2012 raises concerns about serious issues with St George’s Araxa resource.

The visa-section of the Brazilian Embassy in Beijing is currently being inundated with visa applications of Chinese nationals.

Brazilian private investment vehicles are analysing each of the rare earth hopefuls in Brazil in order to place educated bets.

How to view the Brazilian administration placing boulders in the development path of two particularly “Myanmar” junior rare earth miners is hard to say:

Genuine environmental concern?

Or is it something else?

Concerns about a dire water shortage have not yet been raised, which seems odd.

Suspense is rising.

Not what it seems

Exclusive - China issues first batch of streamlined rare earth export licenses, source says

China began designing a new rare earth licensing regime centered around so-called “general licenses” following the late October meeting between Trump and Xi that eased trade tensions between the two countries, Reuters reported in early November.

JL Mag Rare Earth has obtained licenses to ship to nearly all of its clients, while Ningbo Yunsheng and Beijing Zhong Ke San Huan High-Tech secured licenses to export to some of their clients, the person said, declining to be identified due to the sensitivity of the matter.

These are dual-use export licenses for the collateral damage of dual-use rare earth licensing, green-channeling some customers of the 3 companies mentioned. It is the magnet’s content of two rare earths which makes the magnets subject to Chinese rare earth dual-use licensing.

All three are rare earth permanent magnet manufacturers. None of them produces rare earths.

Market manipulation

One of the little observed differences: rare earth permanent magnets are considered high-added value in China and therefore enjoy full VAT refund upon export.

Rare earths are considered low-added value in China and therefore do not enjoy any VAT refund upon export from China.

A discriminatory, market-distorting policy that in our view is fully WTO incompatible. Not only applicable to rare earths, but to all raw materials China dominates.

Resulting from the discriminatory handling material cost of downstream companies are automatically 13% higher outside China than inside China.

Governments act blur

EU bureaucrats do not view this as being substantial. They are blissfully unaware of the fact, that in raw material a cost difference of ca. 3% may well be digestible, but anything above 5% isn’t.

And the US? They don’t have a value-added tax and therefore anything related to value-added tax is viewed being highly suspicious. If the US don’t have it, it should not exist, because there must be something wrong with it.

Why these three companies are treated more equal?

All three are among the largest REPM manufacturers and all three have followed administrative guidance to invest in capacity expansions. Not at their “native” locations but at Baotou, Inner Mongolia, the home of the world’s largest rare earth mine and the seat of China Northern Rare Earth High Tech Group:

Beijing Zhong Ke San Huan is state-controlled, an offshoot of the Chinese Academy of Sciences.

Ningbo Yunsheng’s handicap is that it is private. But it followed Beijing’s administrative guidance. So Ningbo Yunsheng made it to the “good books”.

JL Mag are a favourite of Xi Jin Ping. Innovation near the symbolic location of the beginning of Mao Zedong’s mythical (and thoroughly disastrous) Long March 1934-1935. Xi Jin Ping had visited the factory and he had been pleased. This secured JL Mag a permanent entry in the good books.

Xi Jin Ping at JL Mag on 20 May 2019 Photo: New China News Agency “Xinhua” And no, dear Western Media, JL Mag Rare Earth Co. Ltd. also 6 years later still do not produce rare earths, like all of you falsely reported at the time, without a barest minimum of even basic fact-checking. It is and remains a pure rare earth permanent magnet manufacturer.

Ridiculous

Rare earth prices remain sky-high despite US-China deal

A truce between the U.S. and China over the trade of rare earth metals has not brought down prices from their recent record highs.

The European price for dysprosium stood at $910 per kilogram last Thursday, according to Argus Media, more than triple the level before China imposed export restrictions earlier this year. One kilogram of terbium traded for $3,700, roughly quadruple pre-restriction prices.

Prices for the metals, both used to improve the heat resistance of magnets in electric vehicle motors, have been at their highest levels in data going back to May 2015.

May 2015? Lame. We have data for selected rare earths going back to 1963.

When the prices are low, media complain that China wants to ruin western junior rare earth miners by manipulating prices down.

When prices are high, again there are headlines and “concerns”. Whatever the case, everything is China’s fault. What exactly is the point?

There is nothing negative about high rare earth prices:

High prices encourage new production

High prices encourage substitution

Good and necessary at this time.

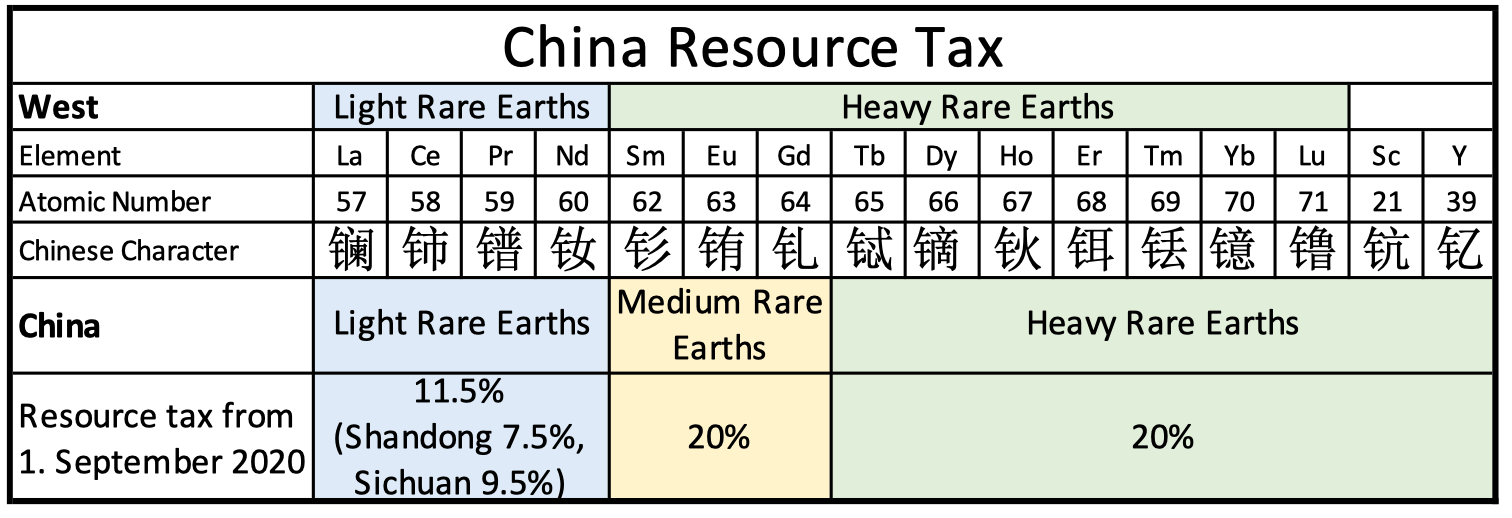

China

Announcement of the Ministry of Finance and the State Taxation Administration on Clarifying the Implementation Scope of Relevant Resource Tax Policies

(excerpts)

III. Regarding the Taxable Objects

(ii) Taxpayers shall pay resource tax on mineral-type rare earth concentrates (including bastnaesite concentrate, monazite concentrate and mixed rare earth concentrate) produced from the mining of light rare earth raw ore through primary processing such as washing and beneficiation, as light rare earth beneficiation products.

(iii) Taxpayers shall pay resource tax on rare earth slurry, rare earth carbonate, rare earth oxalate and mixed rare earth oxides produced from mined ion-type rare earth ore through processes such as ion exchange and oxidation, as well as on medium and heavy rare earth beneficiation products.

V. Regarding related-party transactions

If the price of taxable products sold by a taxpayer to related parties is significantly lower than the price of similar taxable products sold by related parties to other unrelated parties in the same period without justifiable reason, the competent tax authority may adjust the taxpayer’s sales amount of taxable products in accordance with the relevant provisions of Article 3 of the “Announcement of the Ministry of Finance and the State Taxation Administration on the Implementation of Relevant Issues Concerning Resource Tax” (Announcement No. 34 of 2020 by the Ministry of Finance and the State Taxation Administration).

If a taxpayer sells raw ore to a related enterprise, which then processes it into beneficiated mineral products for sale, and the sales revenue of the raw ore is significantly lower than the sales revenue of the beneficiated mineral products sold by the related enterprise after deducting reasonable processing costs and profits, and there is no justifiable reason, the competent tax authority may determine the taxpayer’s sales revenue of raw ore based on the sales revenue of the beneficiated mineral products sold by the related enterprise after deducting reasonable costs and profits.

The legitimate reasons in the above situations mainly include:

(i) Taxpayers who implement government-guided prices, government-set prices, and medium- and long-term transaction prices determined by the price authorities under the prescribed price formation mechanism, as well as statutory price intervention measures and emergency measures;

(ii) Related entities that, in order to protect their own operating costs and profits, sell taxable products at a markup within a reasonable range;

(iii) The price of taxable products sold by related entities includes freight and miscellaneous charges;

(iv) Other legitimate reasons determined by the competent tax authority.

China’s Resource Tax is applied ad-valorem to China domestic mined resources. The tax was implemented in September 2020, as we reported on 5 September 2020.

This clarification limits leeway of taxpayers to define what the “valorem” is and thereby generally increases cost.

China’s Resource Tax does not apply to imported resources. And there is zero import tariff for imported rare earth resources (except USA). Which means it is more attractive to produce based on imported rare earth resources than using resource-taxable domestic resources. An incentive to preserve domestic resources.

Foreign rare earth miners may want to check, if the substantial tax advantage is actually reflected in the price formulas of their Chinese customers.

FAQ:

Why promethium is not featured: It is extinct - which doesn’t stop rare-earth-trading hopeful Traxys to put it on its product list:

There is no scientific definition of light and heavy rare earths. But it is convenient to draw the line between light and heavy rare earths at the “promethium property gap” left behind by the extinct promethium.

EU

RESourceEU Action Plan - Accelerating our critical raw materials strategy to adapt to a new reality

In 2024, the EU has already put forward ambitious measures in the Critical Raw Materials Act (CRMA) ( 2 ). This Act sets clear objectives for EU supply security: by 2030, the EU should have the capacity to extract 10%, process 40% and recycle 25% of the strategic raw materials it consumes (3). In parallel, the EU should diversify its supply so that it does not depend on a single country for more than 65% of its demand.

Well, on the surface this looks like ambitious resolve and bold, great, fearless leadership.

But it is not at all what it seems.

“Clear objectives”

First of all, these objectives are not binding, as the EU can’t impose quota on member states. It refers to overall annual consumption of strategic and critical materials and it does not define percentage of what: Value? Volume?

They also don’t mention what the status quo is. Where are they coming from? What is the base? Relevant regulation requires member states to inform the EU of the base numbers only by 2026. Next year.

Which means there is actually no base for the “clear objectives” set.

Hurray!

The problem with these self-set, anything-but-clear objectives is that the EU can actually already now write the press-release with the hurray announcement, publish it, move on and do something else.

You just torture the underlying data a bit, create an average across all strategic raw materials and volumes and - voila! - you met the objectives and you are already at home.

Aluminium

You don’t believe it? Well, on the “Strategic Raw Materials” list you will find the large volume product aluminium right at the top position. Current values for aluminium volumes in the EU are:

Extraction from bauxite: a tad less than 10%, target almost reached

Processing: 49% of the primary aluminium consumed in the EU is domestically processed, comfortably above the target of 40%.

Recycling: Overall average alu-recycling is estimated to be 69% in the EU, far above the target of 25%

You can guess already, for another example, how copper would look like.

Owing to sheer size, the large volume products will easily make up likely achievement-shortfalls among the smaller products.

Lets move on to the bold action plan.

The bold plan: “Everything also want” (Singlish)

Overall the ambitious action plan caters to the perceived wishes of stakeholders conveniently leaving aside one of the core problems - the elephant in the room - the overbearing Brussels bureaucracy, its much-hated regulations and its inherent inertia.

Here the heads of Brussels’ Christmas wishlist for Santa Claus:

Securing supply with the European Critical Raw Materials Centre

Promoting and accelerating priority projects

2.1 Creating a CRM financing hub to accelerate CRMs projects in the EU and in partner countries

2.2. Leveraging the capacity of Member States and regions

2.3. Operationalising international partnerships toward concrete projects

2.4. Speeding up projects’ delivery

Unleashing the circularity and innovation potential

3.1. Keeping CRMs in the EU and recycling the resources already available

3.2. Incentivising the recycling of critical raw materials

3.3. Stimulating innovation to enable substitution and efficiencies

Increasing European demand for European projects and creating a lasting market

4.1. Enabling demand aggregation and joint purchasing by European industry

4.2. Stimulating CRM diversification by the European industry

4.3. Supporting stockpiling to increase European industrial resilience

Protecting the Single Market and the resilience of the EU CRMs value chain

5.1. Strengthening the monitoring of supply chains and coordinating responses to supply disruptions

5.2. Shielding the EU from hostile interference

Partnering with third countries to diversify

6.1. Reinforcing and expanding the EU’s engagement

6.2. Building on multilateral initiatives to secure diversified supply

“Securing supply with the European Critical Raw Materials Centre” translates to not only a much higher budget but also to more cozy jobs with important-sounding titles for additional functionaries, many of whom member countries desperately want to get rid of by offloading them to Brussels.

“Leveraging the capacity of Member States” is strongly reminiscent of this immortal line:

The man who can smile when things go wrong has always thought of someone to blame it on.

“Protecting the Single Market and the resilience of the EU CRMs value chain”, “increasing European demand for European projects and creating a lasting market” and “unleashing the circularity and innovation potential” means what? More regulation, of course!

After all, how could one possibly expect innovation without more and ever tighter regulation, right?

“So what is the genuinely European contribution to world politics?”, the Swiss Newspaper Neue Züricher Zeitung asks. Here a part of the answer:

Brussels believed it could shape the world more effectively with standards and regulations than Washington could with dollars and military might. This led to monstrosities like the Green Deal and digital legislation. Not to mention the countless directives intended to make the economy more sustainable and ethical, which affect every African smallholder farmer who sells his harvest to a European corporation.

And regulations must be administered. So head-count in Brussels increases, of course.

Lack of sincerity

Where is the permanent disposal facility for radioactive waste from rare earth processing?

What are the arrangements for additional red mud from bauxite processing?

Wait! They may have thought of it! The current EU Commission retires in 2029. A 2030 Rare Earth Waterloo would be on the plate of the new EU Commissioners thereafter. So, all is well.

Our take

This is of course work in progress, but we can already see now how Brussels’ officialdom covers its backside while ensuring continued growth of the bureaucracy.

In our view there must be a very granular product by product approach, preceding any grand plans and “clear objectives”. We would expect to see numerical targets (metric tons) for every single one of the items on the strategic- and critical raw materials lists as the sole and single means of measuring success. All that with an ascertained status-quo, including recognition of the huge stumbling blocks. Anything else would be a complete waste of time.

A plan must include direct, personal responsibility and promotion/bonus-relevance for achieving and missing objectives along the shortest reporting lines possible.

Else all will predictably turn to mush.

No matter what happens, the perpetuation of parasitical EU debating clubs, also known as “initiatives”, is guaranteed.

Meanwhile, also confidence of the general public in the EU bureaucracy reaches ever new lows:

Former EU foreign policy chief arrested in latest scandal to hit the bloc

The arrest of Federica Mogherini, who led the EU foreign service from 2014 to 2019, risked tarnishing the EU’s international image just as it seeks to assert influence in negotiations aimed at ending the war in Ukraine. The EU has been urging Ukraine to tackle rampant corruption.

Authorities in Belgium made the arrests Tuesday after raiding the offices of the EU diplomatic service in Brussels and a college in Bruges. Mogherini now serves as the rector of the College of Europe, a prestigious institute of European studies.

The corruption case targeting Mogherini is the latest to hit European institutions.

Revelations of a cash-for-influence scheme dubbed Qatargate, involving high-profile center-left EU lawmakers, assistants, lobbyists and their relatives, emerged in 2022. Qatari and Moroccan officials were alleged to have paid bribes to influence decision-making. Both countries deny involvement. No one has been convicted or is in pretrial detention, and prospects for a trial are unclear.

In March this year, several people were arrested in a probe linked to the Chinese company Huawei, which is suspected of bribing EU lawmakers.

Last year, the aide of prominent far-right EU lawmaker Maximilian Krah was arrested in a separate case. German prosecutors alleged the aide was a Chinese agent. Krah, who has since switched to the federal legislature of his native Germany, denied knowledge of the suspicions against his former employee.

The sad state of affairs in Brussels.

GE Vernova working with US government to boost stocks of rare earth yttrium - Reuters

GE Vernova - one of only three major makers of gas turbines globally - has yttrium inventories to last the rest of 2025 and into next year, Strazik said, although he did not disclose how long into next year supplies would last.

The company is also investing in alternatives to replace certain rare earths used in production if it became necessary, although there were cost or performance trade-offs in some cases, he added.

That is wonderful, but new supply will not come up this fast. All junior and senior rare earth companies are stubbornly focussed on only the rare earth magnet materials. They have no eyes to see just how important and probably profitable all the remaining rare earths are.

China is overplaying its hand on rare earth materials

In April 2015, after Trump imposed new tariffs, China imposed export controls on rare earth elements and finished magnets, seeking to inflict immediate supply chain pain during negotiations.

Trump only became president in 2017. Alternative fact, anyone?

Friedman’s larger point — that Beijing sees rare earths as negotiation leverage — is consistent with China’s actions. But the U.S. can blunt that leverage through smart investment and policy, without overreacting.

Again the false narrative is being used that rare earths are trade negotiations leverage. We don’t get tired telling you: The rare earth restrictions targeting specifically the US military-industrial complex, announced and implemented on 4 April 2025, have been years in the making. Trade-war or not, these restrictions would have come anyway.

The proposed restrictions of 9 October 2025, implementation postponed to 10 November 2026, were critical mass for trade negotiations.

But that dominance has limits. The rare earth mining base is geographically diverse, and new refining capacity is coming online in Australia, Jordan and even the United States. The War Department recently committed nearly $700 million in loans to U.S. firms — Vulcan Elements and ReElement Technologies — to build domestic magnet facilities that could replace roughly half of current imports within a few years.

The Vulcan and ReElement thing we had covered in our 12 November 2025 issue.

ReElement are licensed to use the Purdue University Ligand Assisted Chromatography For Metal Ion Separation patented process, but originally only for rare earth from coal (ReElements mother company is a coal miner) and recycled resources. For natural resources like monazite Purdue University had originally licensed Medallion Resources, later renamed Gabo Mining and now called Gamma. Since April 2024 ReElements hold the exclusive license to use the patent. Subsequently ReElement has been eagerly courting African monazite miners.

This fringe process is untested on a commercial scale and it is not known if this is commercially feasible at all.

The “investor relations” of Vulcan we had detailed in our post of 27 November 2025.

Recycling and innovations are closing the gap far faster than most analysts expected. Unlike oil or plastics, rare earths can be reused indefinitely. Moreover, recycling rare earth elements is not a dirty process compared to new processing. Companies like Noveon Magnetics can recover them from discarded electronics and other sources, and Apple reclaims neodymium from old iPhones. The global recycling market — roughly $1.5 billion today — is expected to more than double by 2032.

In Minnesota, Niron Magnetics is developing permanent magnets made entirely without rare earths. Its iron-nitride technology performs as well as — or better than — traditional rare-earth magnets at high temperatures. Investors include GM, Stellantis and Samsung. Niron has already broken ground on its first plant.

Fairy tales. We sense a complete disconnect here. Niron is not a prime candidate in terms of high performance permanent magnets.

Rare earth elements from Jordan is unrealistic. It bases on heavy mineral sand’s monazite content, same as in Africa, Brazil, Australia, India, etc. There is no merit to monazite from Jordan. Samples were send to China years ago and that was it.

Then there is Jordan’s phosphate rock for fertiliser, which also holds some rare earth content. Such “combination” attempts have failed before.

But has China overplayed its hand?

Absolutely. NdFeB magnets are 40 years old and they are literally begging for replacement by the next big thing. It really is only a question of time and then the product incorporating more than 90% of all rare earth value will become history.

While China’s supply will be sidelined, except by those customers willing to incur unsustainable risks, rare earths as such will not go away, of course. Far too many applications depend on them.

But rare earths will fade back into the obscurity they originally came from. A tiny, yet important niche of world technology metals.

What could work?

In general it wears people out if they constantly hear about all the projects that just won’t work.

Outlining what could work would require candidates to stop bitching and scratching each other’s eyes out while pan-handling for government hand-outs and vying for largely ignorant investors’ attention.

Cooperation is the order of the day.

Here are select projects that we have some confidence in, standalone or in national combination (this is not investment advice, do your own diligence. All and any projects can fail for numerous reasons at any given time):