More on the Dual-Use Drama; China licenses Malaysia Miners, threatens Korea; Aclara don't hear explosions; Neo Estonia import NdFeB Blanks from China?; White Paper on Magnet Recycling; etc.

Rare Earth 2 May 2025 #174

Note

Stranger from the internet, if you are looking for some sanity in rare earths, then you have come to the right place.

Another long write-up. As Martin Luther said: Here I stand and can do no other.

China’s Minister of Industry & Information Technology

MIIT’s Department Of Raw Materials Industry oversees and manages rare earths in China.

Yet another Minister of Industry & Information Technology has been removed, probably again for corruption, just like his predecessor.

Jin Zhuanglong, who had replaced disgraced Xiao Yaqing in July 2022 as minister and MIIT party secretary, was removed as party secretary at the end of February after a long absence. On 30 April 2025 Jin was also officially removed from the minister post. His successor is Li Lecheng 李乐成.

AI

In view of Sino-U.S. tensions there has been a flood of articles about rare earths. Many of these “expert” articles rely on artificial intelligence, which is not a good idea.

We asked AI about its own weaknesses. The response is worth noting:

Limited understanding: AI models can struggle to understand nuances, context, and subtleties, particularly with language, humour, or sarcasm.

Lack of common sense: AI models can make decisions or take actions that are not sensible or practical in real-world situations.

Limited domain knowledge: AI models may not have the same level of domain-specific knowledge or expertise as humans.

To put it more plainly, by its own admission, AI is inherently stupid. Which sums up quite nicely what is wrong with all recent AI-reliant write-ups about rare earths.

Come to think of it, the Pentagon developed an AI system for solving the U.S. critical metals problem. Now, that explains….

Good stuff

But apart from that, also great quality content is coming out, related to the unusual situation. Take, for example, A Semiconductor Rare Earths Problem? on YouTube by fellow substacker Asianometry. Or Comparative Analysis of U.S. Tariffs on Products from Selected Countries by fellow rare-earthling Daniel Mamadou.

Potential death knell to junior IAC miners

China has begun licensing restricted IAC leaching technology to Malaysian IAC miners. Technology, that these miners already had, informally.

China’s likely objective: limiting China market access to only China-licensed IAC miners. Read the full story regarding Xi Jin Ping’s visit to Malaysia below.

Holidays

From May 1 (Labour Day) and thereafter up to May 9 is the Golden Week holiday in China. Typically the country hibernates during the Golden Week.

But this time people at China’s Ministry of Commerce and China Customs probably will do overtime doing damage control, rather than frolicking in Thailand.

Pre-holiday rare earth prices headed south.

Want another Pearl Harbour?

Bloomberg reported on 29 April 2025:

The Chinese exempting some goods from tariffs indicates they are interested in reducing tensions, Bessent said, adding that he has “an escalation ladder in my back pocket and we’re very anxious not to have to use it.” Escalation could include an “embargo,” he said.

Bessent might want to read up about “ABCD Encirclement” embargo of 1940. The trade sanctions back then were going to cause an economic collapse of Japan.

Enter the surprise attack on Pearl Harbour in 1941. Perhaps not as much of a surprise.

More on the Dual-Use Drama

Captain Edward Aloysius Murphy, one of the great American philosophers of the 20th century, is grossly underrated in China.

After the cock-up with gallium and germanium two years ago, China’s politicians seemed to have had unshakable confidence that all would work as designed this time around when declaring 7 rare earth elements subject to dual-use licensing under China’s obligations from the Nuclear Weapons Non-Proliferation Treaty.

Fat hope.

Much rather the implementation of China’s new dual use regulation for 7 rare earth elements has turned out to be a real crowd-pleaser.

The intention had been to specifically target and hit U.S. defense industries. Instead they hit everyone on the planet, including themselves.

Captain Murphy’s core thesis has again been proven beyond reasonable doubt:

Anything that can go wrong, will go wrong.

Magnet standstill

A blogger in China under the pen name Sunset in Xicheng Lane 西城巷斜阳, quite possibly central CCP propaganda unit or related to one, self-describes the mess in its latest blog entry:

Nidec Group's motor production line has come to a standstill. This company, which supplies core components to Toyota and Honda, was forced to postpone the delivery date by three weeks because it could not obtain Chinese neodymium iron boron magnets on time. More seriously, Chinese customs data showed that the export volume of rare earths in the first 20 days of April fell 68% year-on-year, of which EU shipments fell 73%, and the inventory of rare earth magnets urgently purchased by US military enterprises was less than two weeks.

Only someone with direct access to China Customs live data could possibly know this, mere mortal can’t. And the samarium-cobalt inventory of US defense contractors? Sunset in Xicheng Lane must have been diligently counting for a while to figure that one out.

The blog entry goes on to say:

The United States tried to rebuild its domestic production capacity through policy support, but the reality is cruel: MP Materials' Mountain Pass mine in California will only produce 45,000 tons of rare earth oxides in 2023, accounting for only 15% of global demand, and all of it needs to be shipped to China for refining. Even so, the company plans to invest $700 million to build a magnet factory, which will not be put into production until 2027 at the earliest. What's more fatal is that China holds 90% of the patents for rare earth centrifugal extractors, which can purify 17 rare earth elements to 99.9999%. This technical barrier makes it difficult for the United States to break through.

Accounting for 15% of global demand? When gunpowder was invented in China, this guy can’t have been anywhere near.

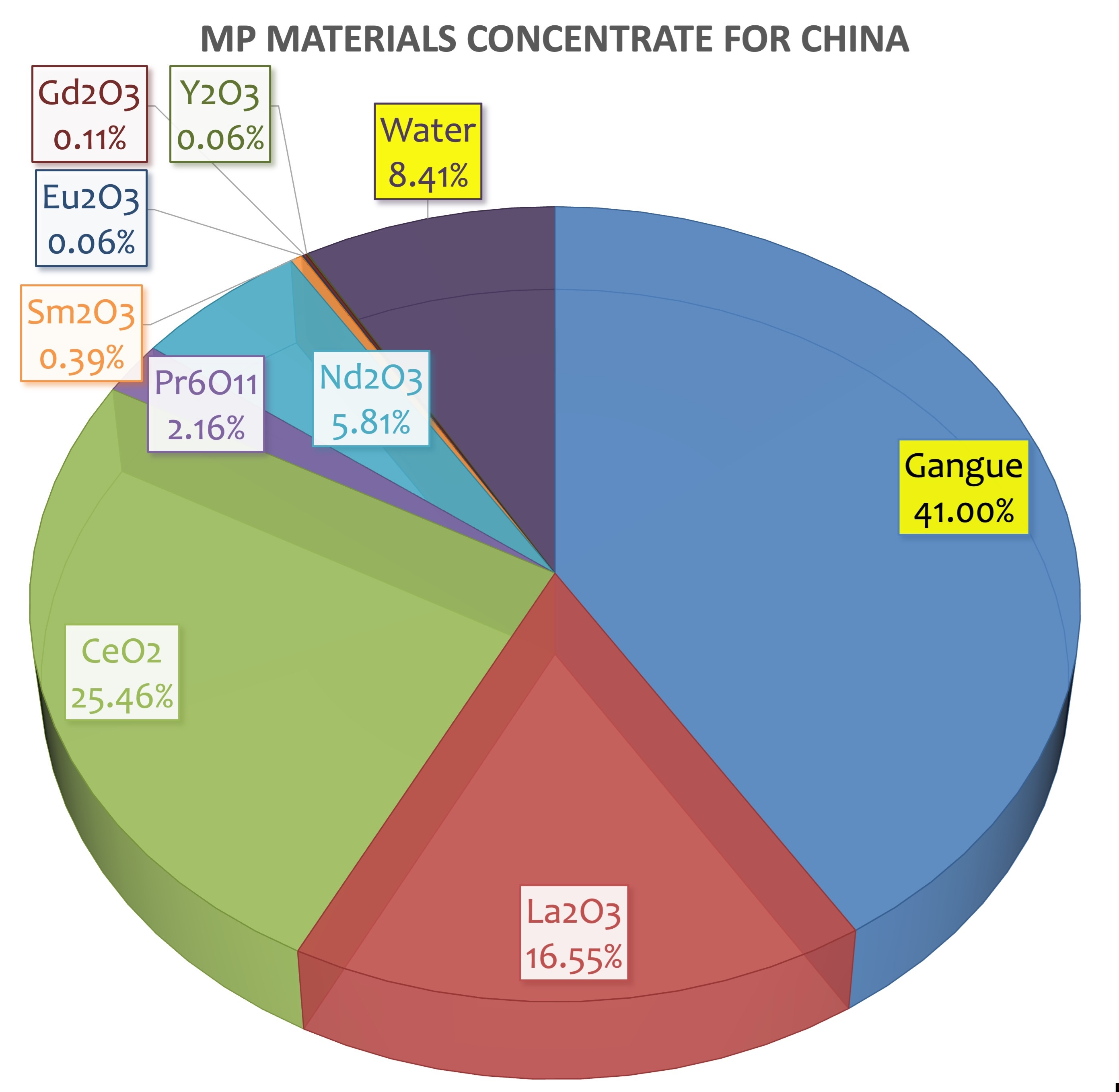

Fact check: MP’s 45,000 t of TREO

This is the composition of a sample of what MP Materials ship to China:

Accordingly ca. 80% of the TREO MP Materials ship to their Chinese masters consists of lanthanum and cerium. The world needs additional lanthanum and cerium from MP Materials as much as all of us need a 3rd shoulder. MP contributes to global oversupply of La/Ce.

Only ~16% or ca. 7,200 t of the 45,000 t TREO MP ship to China is much-hyped NdPr, in its unseparated form for the sole and single application in NdFeB magnets.

Considering a NdPr recovery rate of 65% (China claims it is higher) these 7,200 t shrink to 4,680 t or just about 4.5% of world NdPr demand 2024.

MP could only separate 1,300 t of NdPr last year, when they ran an impressive operating loss of US$0.73 per US$1 of revenue. Lynas produced more than 4 times more of non-radioactive NdPr - at a profit.

George Carlin used to put it this way:

America’s leading and most profitable industry is still the manufacture, packaging, distribution and marketing of b*llsh*t. High quality, Grade A, prime-cut, pure American b*llsh*t.

Screaming headlines like “China faces 60% drop in rare earth concentrate imports” by the purveyors of rare earth hype should be re-evaluated accordingly - but then it would not be hype anymore. Refer to the Price section below, how the current situation plays out in prices.

And bovine brown matter brings us straight to:

99.9999% 6N pure metal

The metal purity sounds great, but don’t be intimidated. The Chinese measuring standard is the metal purity contained in 99% TREO, not in the total mass. A slight but rather significant difference, particularly if you boast 6N.

Example an excerpt of the Chinese dysprosium metal industrial standard GB/T-15071:

No licensing of Chinese NdFeB patents

While good at data, Sunset in Xicheng Lane seems to be unaware of important facts.

The relevant technology had already been classified as prohibited for foreign technology transfer/licensing from China 24 years years ago:

China’s Export Prohibited / Export Restricted Technology Catalogue (中国禁止出口限制出口技术目录):

Item No. 083201J (08=since 2008, J=prohibited) - actually this item has already been in the catalogue since 2001:

1. Rare earth extraction and separation technology

2. Production technology of rare earth metals and alloy materials

3. Preparation technology of samarium-cobalt, neodymium iron boron

and cerium magnets

4. Preparation technology of rare earth calcium oxyborate

Mao Zedong: Socialism thrives on contradiction

For over a decade, China itself exhausted all legal avenues in its fight against Japan's Hitachi Metals (now Proterial) regarding the company's selective licensing policy for its sintered NdFeB magnet patents.

Now that the table has turned, why would China’s officialdom even begin to think that the West would put up with rare earth patents that are not licensable abroad because of trade-restrictive Chinese law?

During COVID-19 exceptions from global IP protection were discussed, as well as compulsory/forced licensing. Has Sunset in Xicheng Lane any ever so remote doubt, that foreign governments might go down this avenue?

Benighted

The entry concludes with:

The outcome of this contest has begun to emerge: the China Nonferrous Metals Industry Association pointed out that export controls will not affect compliant trade, and Chinese rare earth companies will continue to deepen international cooperation. The report of the US think tank CSIS warned that if the West cannot break through China's technological blockade, its competitiveness in new energy vehicles, robots and other fields will regress by ten years.

First of all, as the blog describes itself, the export controls evidently already do affect compliant trade.

Evidently Sunset in Xicheng Lane does not consider, that China has just ruined it’s hard-won reputation as a dependable supplier. It will have tangible consequences. No instant gratification, but medium and long term impact.

Sino-Japanese rare earth JVs as well as Solvay’s wholly-owned rare earth separation factory in China will also not be happy of state-interference in what should be their own affairs and their own products.

In our view China’s government grossly underestimates what is in the West’s rare earth pipeline, because China’s officialdom is distracted by all the noise of largely useless rare earth wannabes in the West.

Origin of Sunset in Xicheng Lane

Considering that the blog is posted in Guangxi, the name probably refers to Xicheng Lane in Liuzhou City, Guangxi Province, home of the important 75th Group of the People’s Liberation Army.

Other China industry comments:

Rare earth magnet industry giant Zhenghai Magnetic Materials say:

For many years, the company has been committed to the research and development and production of products such as zero-heavy rare earth magnets, low-heavy rare earth magnets, and ultra-light rare earth magnets.

…neodymium iron boron magnets without heavy rare earths are not within the scope of export control. The company's production and operation are currently normal.

SME magnet distributor Karuiqi writes:

First, the types of magnets subject to control include samarium cobalt permanent magnets (such as samarium cobalt alloy targets, samarium cobalt magnets), neodymium iron boron permanent magnets containing terbium or dysprosium, and other magnets made of alloys and oxides containing rare earth elements (such as gadolinium, lutetium, scandium, yttrium and other rare earth elements). These magnets containing specific rare earth elements are subject to export control.

For products that do not contain controlled rare earth elements, such as ceramic ferrite magnets and alnico magnets, there are no restrictions in theory, but the current customs system may misjudge [it does] due to policy adjustments, resulting in temporary detention or inspection delays. Some companies have successfully exported magnets that do not contain controlled rare earths by air, but there is still uncertainty about sea transportation.

According to relevant reports, customs currently prohibits not only the export of heavy rare earth metals and magnets to the United States, but also prohibits the export of heavy rare earth metals and magnets to any country including Japan and Germany.

Magnet distress

As described above is distress in the rare earth permanent magnet supply chain, which we attribute to a mishap in China’s online dual-use licensing system.

First a few facts:

China exported 58,147 t of NdFeB magnets to 130 countries worldwide in 2024

China’s capacity for producing rare earth permanent magnets in 2024 exceeded 515,000 t

Notwithstanding work-in-progress and inventory, it means that roughly 80% of NdFeB produced in China are locally consumed in China.

About half of the NdFeB magnet output are commodity magnets with a working temperature limitation of 80℃ for consumption in everyday products in 130 countries worldwide plus China

The magnets which the western media keep hyperventilating about are high performance, high working temperature NdFeB magnets, highly engineered products tailored to the specific needs of each individual customer, incl. the currently fashionable deemed high growth applications, electric vehicles and wind turbines. Obviously not commodities.

China’s dual-use licensing for the 7 rare earth elements also includes all products, where these elements might be contained

China’s dual-use regulation includes dysprosium and terbium, which are not contained in commodity NdFeB magnets.

Commodity NdFeB therefore do not fall under the dual-use licensing system

But dual-use dysprosium and terbium are essential alloys for high performance, high working temperature NdFeB magnets fall under the regulation.

China’s harmonised system code, at the core of the online dual-use licensing IT system, does not distinguish between commodity NdFeB magnets without Dy and Tb and high performance, high working temperature NdFeB magnets alloyed with Dy and Tb.

And thus we have arrived at the current mess.

MOFCOM must find a way to distinguish among the 307 million pieces of NdFeB magnets China exported to the U.S. in 2024 (as per statistics of USITC), which ones were likely to be used by U.S. defense contractors. Good luck with that.

Additionally MOFCOM is flooded with license applications, including products for applications that no-one had anticipated.

In view of China’s outsized capacity plus add-on capacity under construction, assuming that China wants to stop export of these magnets is not reasonable.

Price-mongering

Western consultants out there, who make a living of continuously forecasting sky-high rare earth prices in order to make junior rare earth miners’ feasibility assessments look beautiful, predict a lasting rare earth boom.

We would recommend caution. Here is the change of core rare earth prices over more than 6 decades, which include China’s heavy-handed restrictions before 2014:

Of course there were different fashionable applications at different times for different rare earth elements:

NdFeB relevance

Current Nd and Pr prices are lower than 1993. The older ones among us may recall the unprecedented electronics boom in the beginning of the 1990s, exactly around the time when - thrilled by the then strong market performance - Deng Xiao Ping said “Middle East has oil, China has rare earths.” It was not long-term planning, foresight and communist conspiracy, like certain junior rare earth miners like to spread in their shallow corporate fog.

Kudos: Fastmarkets nailed it

During a recent event of EIT Raw Materials rare earth market expert Caroline Messecar of Fastmarkets on her timeline presented exactly, what is going on:

Whenever magnet rare earth prices rise, demand is breaking off.

Why?

As described before, while there are applications for which the NdFeB magnet is essential, the bulk of the NdFeB market are commodity magnets for everyday applications. In many of these applications NdFeB magnets are nice to have, but not without instantly available substitute.

There was life before the NdFeB magnet - and there will be life after

Even in much hyped wind turbines the expensive high performance, high working temperature NdFeB magnet is subject to a cold, hard calculation: NdFeB-based turbines may be more energy efficient and need less maintenance, but there is always a trade-off of its cost to other, traditional, cheaper turbines. While offshore low maintenance is definitely a driver of NdFeB-based turbines, on land this is not necessarily so.

5 years ago we asked Vestas, how many of their wind turbines contained NdFeB magnets. The answer was Vestas had none, nil, zilch, zero, nada, nothing.

Nowadays Vestas sports NdFeB-based wind turbines, but it keeps its previous solutions on hand, which can be more feasible than NdFeB-based solutions.

Even automotive reacts negatively

Since the large contracts in NdFeB are based on rare earth price pass-through, any change in rare earth pricing hits the magnet maker and thereby his end-user directly and almost instantly.

Anyone who ever had a supply contract with Big Auto knows perfectly well, in order to “get in” you must commit to cost improvements of 5-15% per year, depending on the category of product. No automotive maker with mass-production will put up with capricious component cost.

If the long term prospect is a doubling or tripling of prices, the component drops out and it will be substituted.

And, as we have pointed out several times, there are nice substitutes of NdFeB also for EV motors. Just take Proterial’s ferrite-magnet-based motor or BMW’s rare-earth-free drive train.

China dominates ferrite magnets, too, but it is fully import-dependent on strontium, a must-have for ferrite magnets:

At present, China's strontium products have few varieties, low output, and low quality. The mainly low-end products based on industrial-grade strontium carbonate and industrial-grade strontium chloride compounds. Most of the high-end strontium compounds need to be imported from abroad.

Yes, yes, yes, the NdFeB offers first class energy efficiency and power, light weight and whatever.

But if you ever moved in your NdFeB-powered Tesla through downtown Toronto or London (UK) at anywhere between walking-speed and the speed limit of max 30 km/h, you will come to realise that there is actually no need for a mass-produced family vehicle with 400 horse powers owed to the high performance, high working temperature NdFeB magnets in the motor.

Likewise on highways. At a speed limit of 110 km/h or even lower, the usefulness of a mass-produced family vehicle that accelerates from 0 to 100 km/h in under 5 seconds is somewhat limited.

It is likely that Big Auto will limit technological leadership to it’s high-end electric vehicles and use the resulting hi-tech image for more practical, market-adequate, mass-produced vehicles.

Anyway, the popularity of hybrid vehicles over fully electric vehicles already helps normalise glowing forecasts by the usual suspects of sintered NdFeB inter-galactic consumption growth.

Everyone in China’s rare earth business understands all this full-well. But in the West people are still at the beginning of the learning curve.

White paper on magnet recycling

Dr. Fernand Vial and Dr. John Ormerod (JOC LLC) published a white paper on recycling of rare earth permanent magnets to point out risky shortcuts in magnet recycling.

It applies to concepts of at least three U.S. projects and several more in the EU.

If you are a prospective investor in magnet recycling, you really want to read and understand this short white paper.

And you might want to refer to Momentum Technology’s Preston Bryant’s recent post on LinkedIn on rare earth permanent magnet recycling:

1. Where are they getting the feedstock?

If they say “end-of-life devices,” press harder.

Small magnets are notoriously difficult to recover, they’re embedded in consumer electronics that almost always get shipped to Asia for a second life.

And if they’re talking about large magnets (from wind turbines or MRI machines), know this: there’s already a thriving direct reuse market for the big ones. These magnets are rarely recycled, they’re remanufactured or reshaped and reused by the OEMs themselves. The material never touches the open market…..

Humanoid robots are the future!

Another current topic of rare earth hypists is the universal introduction of the humanoid robot to the world’s greying societies. Never mind the fact, that outside North America many - if not most - people do not have the space in their homes for such clunky equipment. Just look at Japan, Korea and the EU and realise, that the mass market for this product may be a bit limited.

Unitree Robotics are deemed to be the most advanced in humanoid robots in China and are also ahead of Boston Robotics.

Watch here the Unitree humanoid robot performing at the starting line of the first Humanoid Robot Half Marathon in Beijing, a propaganda event of China’s CCTV and New China News Agency, on 19 April 2025:

Few aged people will be able to resuscitate their robotic domestic helper.

6 of the 20 robots finished the 20 km marathon. Only one made it within the cut-off time of 3.5 hours and had not been been swapped against a backup.

In robot evolutionary terms these robots may well be at the development stage of Windows 98, May 1998. The famous Blue Screen of Death:

Source: Lingua Sinica

Rare Earth Technology

Preparing for a recent presentation about China’s rare earth related export restrictions - which also details U.S. defense industries dependence on each of the dual-use rare earth elements - we found:

The China Export Prohibited / Export Restricted Technology Catalogue of 2001 contained a blanket prohibition on all and any rare earth related technology transfer abroad.

Circumstantial evidence, however, points at this ban having been in place already since 1998.

The 2008 version of the catalogue spun-off and moved ion-adsorption clay (IAC) mining know-how from the prohibited category to the restricted category, suggesting that under certain circumstances foreign transfer of this environmentally extremely harmful technology export might be permissible.

Also some other basic rare earth know-how was spun-off from the one-fits-all of 2001 and moved from prohibited to restricted in the 2008 catalogue.

This came along with early ventures of Chinese entities into the foreign rare earth space - for example 25% shareholding in Arafura Rare Earths in 2009.

And in 2014, after China had banned IAC mining within its jurisdiction, Chinese IAC experts moved to Myanmar together with thousands workers (who are now also active in Laos and Malaysia), bringing with them “restricted” rare earth know-how.

The changes from the prohibited to the restricted category in the catalogue gave Chinese rare earth companies the opportunity, subject to permission, to offer help with exploiting rare earth resource abroad and ship the resulting concentrates and intermediate products to China.

Status quo

The status quo is that there are downstream high-added value rare earth technologies in the restricted category that may be licensed for foreign technology transfer under undisclosed conditions. Perhaps significant Chinese ownership of shares in the foreign entity or tangible Chinese control is among the conditions (see MP Materials).

But the rare earth compounds and metals for use in many technologies are basically only available from China.

China’s presidential visit to Malaysia

Unbeknownst to USGS, who incomprehensibly base their Malaysia rare earth resource assumptions on “reported import data for China”, every Malaysian state but one has some ion-adsorption clay rare earth deposits. Related to that Malaysia’s government has been pestering China for rare earth know-how for years.

Xi’s promise

China’s president visited Malaysia from 15 to 17 April 2025. Regarding general observations of China’s strategy at play we recommend the opinion piece Red Strings Attached: How China Is Quietly Rewriting Malaysia's Future by fellow substacker dissedalis.

According to Malaysia’s Foreign Minister Datuk Seri Mohamad Hasan on 17 April 2025, Xi Jin Ping had personally agreed to sharing rare earth know-how with Malaysia.

Xi Jin Ping brought presents

Actually, technology transfer licenses to Malaysian rare earth miners had already been issued in preparation of Xi Jin Ping’s visit to Malaysia and they were sent out right after.

Informal technology transfer

In view of the “catalogue”, China offers know-how to Malaysia that has already permeated from China via Myanmar to Malaysia and Laos anyway, (know-how that is on China’s National Development & Reform Commission “elimination list”, see below).

The General Research Institute of Nonferrous Metals (GRINM) magnesium sulphate leaching know-how, far less environmentally impactful, has already been independently and seemingly successfully evaluated by Brazilian Critical Minerals.

In our view this technology transfer would likely improve the Malaysian miners chances of exporting primary raw material to China, which is China’s primary objective.

Please refer to Aclara in the Companies section below for more details on mixed rare earth carbonate vs. mixed rare earth oxide and why we think mixed rare earth carbonate is on its way out.

The downside: a coup de grace for foreign IAC hopefuls

We expect China to limit market access to foreign suppliers to only those, whose Chinese know-how has been properly licensed. And who China licenses, is China’s choice.

Brazil, the “B” in BRICS, and China enjoy currently good relations from one socialist government to another socialist government. Going forward Australian-owned IAC hopefuls in Brazil may still run into an unforeseen problem: No technology license from China quite possibly means no China market to sell to.

Transferred technology to be eliminated in China

Meanwhile, core elements of in-situ leaching of IAC deposits are on the elimination list of China’s state planner, the National Development & Reform Commission. See below.

Forgotten by the media but relevant

Guidance Catalogue for Industrial Structure Adjustment (2024 Edition)

The "Catalogue (2024 Edition)" consists of three categories of catalogues: encouraged, restricted and elimination. The encouraged category mainly refers to technologies, equipment and products that have an important role in promoting economic and social development; the restricted category mainly refers to backward processes and technologies that do not meet the industry access conditions and relevant regulations, are not conducive to safe production, and are not conducive to achieving the carbon peak and carbon neutrality goals, and need to be supervised for transformation and the prohibition of new production capacity, process technology, equipment and products; the eliminated category mainly refers to backward processes and technologies, equipment and products that do not meet the relevant laws and regulations, seriously waste resources, pollute the environment, have serious safety hazards, hinder the realisation of carbon peak and carbon neutrality goals, and need to be eliminated.

Rare earth relevant content:

ENCOURAGED

V. New Energy

1. Wind power generation technology and application:

Technology development and equipment manufacturing of offshore wind turbines of 15MW and above, floating offshore wind power technology, construction and equipment manufacturing of wind farms in plateaus and mountainous areas, construction and equipment and submarine cable manufacturing of offshore wind farms, and application of rare earth permanent magnet materials in wind turbines.

IX. Nonferrous Metals

4. New materials:

Information technologyElectronic-grade polysilicon for semiconductors and chips (including polysilicon materials for zone melting), silicon single crystals (diameter of 200 mm or more) and silicon carbide single crystals, silicon-based electronic gases, indium phosphide single crystals, polycrystalline germanium, germanium single crystals, etc., CZ-pulled compound semiconductor materials with a diameter of 125 mm or more or horizontal growth with a diameter of 50 mm or more, large-scale high-purity targets such as aluminum, copper, silicon, tungsten, molybdenum, and rare earth, ultra-high-purity rare metals and targets, copper-nickel-silicon and copper-chromium-zirconium lead frame materials for ultra-large-scale integrated circuits, electronic solders, etc.

Transportation

High-end manufacturing and other fields. Light alloy materials, copper-nickel metal materials, rare earth metal materials, precious metal materials, composite metal materials, metal ceramic materials, auxiliary materials, biomedical materials, catalytic materials, 3D printing materials, high-performance carbide materials and their tools for high-end manufacturing such as aerospace, marine engineering, CNC machine tools, rail transportation, nuclear engineering, new energy, advanced medical equipment, environmental protection and energy-saving equipment.

Green mining

Efficient, green, low-carbon mining and mineral processing technologies (agents), stripping backfill (filling) technologies, low-grade, complex, and difficult-to-process mineral development and comprehensive utilization technologies and equipment, extraction of valuable elements from symbiotic and associated minerals and comprehensive resource utilisation technologies, green and efficient leaching integrated technologies for ionic rare earth ores, and development and application of advanced and applicable technologies for conservation and comprehensive utilisation of mineral resources [China’s Comprehensive Resource Utilisation Policy is also at the core of rare earths].

RESTRICTED

VII. Nonferrous metals

1. New construction and expansion of tungsten mining projects with tungsten metal reserves of less than 10,000 tons (except for deep and marginal resource mining and expansion projects of existing tungsten mines), tungsten, molybdenum, tin, and antimony smelting projects (except for projects that comply with national environmental protection and energy conservation laws and regulations), antimony oxide, lead-tin solder production projects, rare earth mining, smelting and separation projects (except for rare earth enterprise group projects that meet the requirements of the total amount control indicators of rare earth mining, smelting and separation)

Note: “Control indicators of rare earth mining, smelting and separation” refers to the rare earth quota of the Ministry of Industry & Information Technology (MIIT).

TO BE ELIMINATED

VI. Nonferrous metals

20. Heap leaching and pool leaching [in-situ leaching] technology for ionic rare earth ores

21. Development projects of single monazite minerals [banned since 2012]

22. Process projects for preparing metals by electrolysis of rare earth chlorides

23. Development projects of mixed rare earth mines with an annual output of less than 20,000 tons (REO) per year, development projects of bastnaesite rare earth mines with an annual output of less than 5,000 tons (REO) per year, and development projects of ionic rare earth mines with an annual output of less than 500 tons (REO) per year

24. Rare earth separation projects with an annual output of less than 2,000 tons (REO) per year

25. Light rare earth metal smelting projects with an annual output of less than 1,500 tons, an electrolytic cell current of less than 5,000A, and a current efficiency of less than 85%

Note that different from other items in the elimination category, there is no time limit set for the above rare earth related eliminations. Actually, single element monazite mining had been banned in 2012 already. There is some beach sand monazite mining along the southern China coastline, but that monazite is part of heavy mineral sands, mixed, not single element.

Separately, strictly enforced numerical targets apply to the emissions of all elements of China’s rare earth industry.

For better understanding that the NDRC does mean business:

Investment in elimination projects is prohibited. Financial institutions should stop all forms of credit support and take measures to recover loans already issued; all regions, departments and relevant enterprises should take effective measures to eliminate them within the prescribed time limit…. During the elimination period, the national price authorities may increase the power supply price. Production technology, equipment and products that have been eliminated by national orders shall not be imported, transferred, produced, sold, used or adopted.

For enterprises that fail to phase out production technology, equipment and products on schedule, local people's governments at all levels and relevant departments shall order them to stop production or close down in accordance with relevant national laws and regulations, and take appropriate measures to relocate enterprise personnel and safeguard the credit assets of financial institutions; if their products are subject to production license management, relevant departments shall revoke their production licenses in accordance with the law; environmental protection management departments shall revoke their pollution discharge licenses; power supply companies shall stop supplying electricity in accordance with the law. Those who violate the regulations shall be held accountable in accordance with the law.

Media incompetence

Myanmar earthquake may have disrupted China’s rare earth supplies, analysts say

Keep reading with a 7-day free trial

Subscribe to The Rare Earth Observer to keep reading this post and get 7 days of free access to the full post archives.