If RE or only the weather - everything is national security in China; RE forecasts in doubt; 3rd batch of China quota; RE stock performance 2024; Korean CEO at VTRE; and more...

Rare Earths 17 December 2023 #134

Roughly 50% of goods imported into the United States contain REE, valued at approximately $1.2 trillion dollars.

US Department of Energy (2018)

Reuters

Insight: Western start-ups seek to break China's grip on rare earths refining

China began to rapidly expand in the industry starting during the 1980s and now controls 87% of global rare earths refining capacity, according to the International Energy Agency. That prowess has helped propel the country's economy to the second-largest in the world.

Emerging Western rivals now offer the tantalizing prospect of processing the minerals in faster, cleaner and cheaper ways, if they can successfully launch.

"The existing rare earths refining process is a nightmare," said Isabel Barton, a mining and geological engineering professor at the University of Arizona. "That's why there are so many companies promising new methods, because we need new ones."

Interviews with nearly two dozen industry consultants, academics and executives show that if one or more of these novel processing technologies succeed as hoped by 2025, they could slash reliance on Chinese rare earths technology and its toxic by-products while also bolstering plans by Western firms to charge premium prices for the strategic minerals.

Several rare earthlings took issue with this write-up, accusing it of bordering on sponsored content, full of falsehood and poorly researched.

One rare earthling remarked:

Ernest sticks to a click-bait sensationalist narrative without presenting a single shred of economic analysis or any discussion of -or evidence as to- what is so “toxic” or such a “nightmare” with SX. The two currently largest Rare Earth SX operators outside China, Neo and Lynas, have achieved the highest sustainability ratings (Gold - as audited by outside auditors) for their operations.

Surely myths need to be debunked, like China’s rare earth “export embargo” 2010/2011, which was rather an unintended result of bureaucrats’ gross incompetence than purpose, or the myth of China purposefully dumping rare earths in order to cripple foreign miners, after it had spent decades on trying to bring rare earth prices up, not down.

However, this sector has risen from complete obscurity 20 years ago. No matter how ignorant, write-ups keep interest in the sector alive. Keeping the public interested is the life-line of junior rare earth miners.

What is happening to RE and RE magnet exports?

The Global Rare Earth Industry Association (REIA) published this chart, showing that China’s exports of rare earths and rare earth permanent magnets are flat:

Where is the growth?

Consultants keep lecturing everyone and sundry about the forecast stellar demand growth of rare earths.

What they do not tell you is, that this demand growth occurs in China and in China alone. Because it is China, where practically all rare earth permanent magnets are made, which in turn represent more than 90% of rare earth output value.

The enormous demand growth forecasts of rare earths rest on only one product, and on only two principal growth pillars:

The NdFeB rare earth permanent magnet for

e-mobility, and

wind turbines.

If only one of these two pillars fails to deliver, the high rare earth demand forecasts will falter.

We think both pillars are taking a hit. Read on.

Pillar I: e-mobility

Electric mobility should be growing and pumping up demand for magnets, wherever principal automotive companies are located.

Consequently, an innocent observer would expect China’s exports of rare earth permanent magnets to the West to sharply increase.

Exports flat

After increasing from 32,696 t (2018) to 53,135 t (2022), China’s rare earth permanent magnet exports are not expected to grow year-on-year in 2023.

While China’s exports of NdFeB magnets to the U.S. are set to increase 15% in 2023, exports to Japan and the EU have fallen flat.

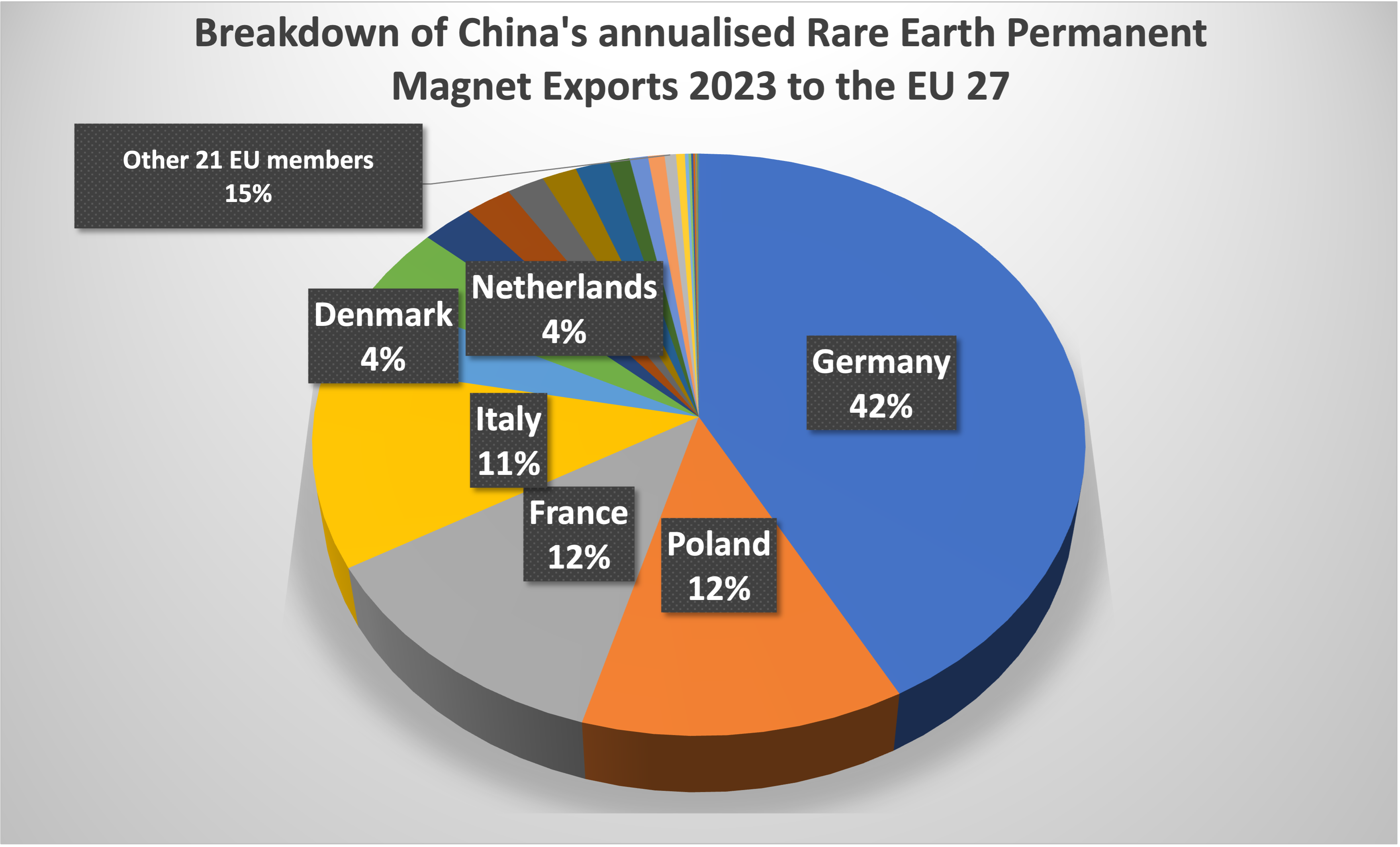

>40% of China’s rare earth permanent magnet exports head for the EU

China’s most important export market for NdFeB magnets is the EU.

NdFeB magnet exports from China to the EU increased from 12,472 t (2018) to 21,074 t (2022). However, for 2023 we expect to see only 4% year-on-year growth (2021: +35% yoy, 2022: +23% yoy).

Why has growth slowed down?

Germany is the largest destination for China magnets within the EU27

Within the EU, Germany is the main destination for China’s rare earth permanent magnets. Germany alone is good for roughly 10,000 t/year or almost 20% China’s exports of NdFeB magnets.

But NdFeB exports to Germany may only grow 3.5% in 2023. This is not a short-term setback, it may actually become a prolonged situation.

Germany is stalling

The coalition agreement of the current German government of Social Democrats, Greens and the Liberals obliges the government to aim for 15 mio fully electric vehicles on German roads by 2030.

This target looks ever more unreachable:

The current number of registered EV in Germany is 1.3 mio. In order to reach the target of 15 mio EV by 2030, 65% of the ca. 3 mio new registrations per year should be EV;

Out of a total of 2.6 mio newly registered vehicles in Germany between January and November 2023, 469,565 were EV . 18%, not 65%;

Compared to the same month last year, the number of newly registered EV in Germany dropped 22.5% during November 2023.

In all likelihood the 2022 to 2023 growth of newly registered EV in Germany will be zero.

Consequently, Germany’s automotive industry thinks that there could be maximum 9 mio EV on German roads by 2030, instead of the targetted 15 mio. Even the lower number sounds quite optimistic.

Now, of course Germany is not a self-contained market. But its problems affect every EV seller in the EU’s largest market, no matter if German or foreign.

Challenges

Here are the reasons for this trend in Germany:

Compared to equivalent internal combustion engine cars, EV prices are 10-12% higher in Germany;

There are only 3 models of EV below EUR30,000 available in Germany, none of them produced by a German automotive company;

Charging an EV costs about the same as filling the tank of an internal combustion engine car;

There are more than 2,000 charging station operators in Germany, all of them with different payment modes and payment apps;

Germany’s power grid can’t take it. Urgently required changes and additions need permits, which in average take between 8 and 10 years to obtain;

Half of Germany’s counties have no public charging stations;

Expiry of EV subsidies: On 17 December 2023 Germany ended all buyer subsidies for EV.

All issues which could be tackled by determined policy, but there is a massive problem. Read on.

Illegal budget

The German debt-ceiling, the limit on the ability to raise new debt, is edged in stone in Article 109 of the German constitution, the “Grundgesetz” (basic law).

During COVID the German government had raised emergency funds beyond the legal debt-ceiling, which had been permissible because of a state of emergency having been declared.

The coalition government tried to re-allocate EUR60 bio of these emergency funds to the Climate Transformation Fund budget for 2024. This was judged unconstitutional by Germany’s constitutional court, leaving a gaping hole in the 2024 budget.

German climate-measure funding 22% below plan

Instead of having more funds to address aforementioned EV issues, there will be less.

In the new attempt to create a budget for 2024, the Climate Transformation Fund is likely to be cut by at least EUR12.7 billion. Originally EUR57.6 billion for 2024, the funding will now be less than EUR45 billion.

Within this fund, originally EUR4.7 billion had been earmarked for the further development of e-mobility including the expansion of the charging infrastructure in 2024.

The troubles are not limited to the EV sector. And this brings us straight to the second demand growth pillar:

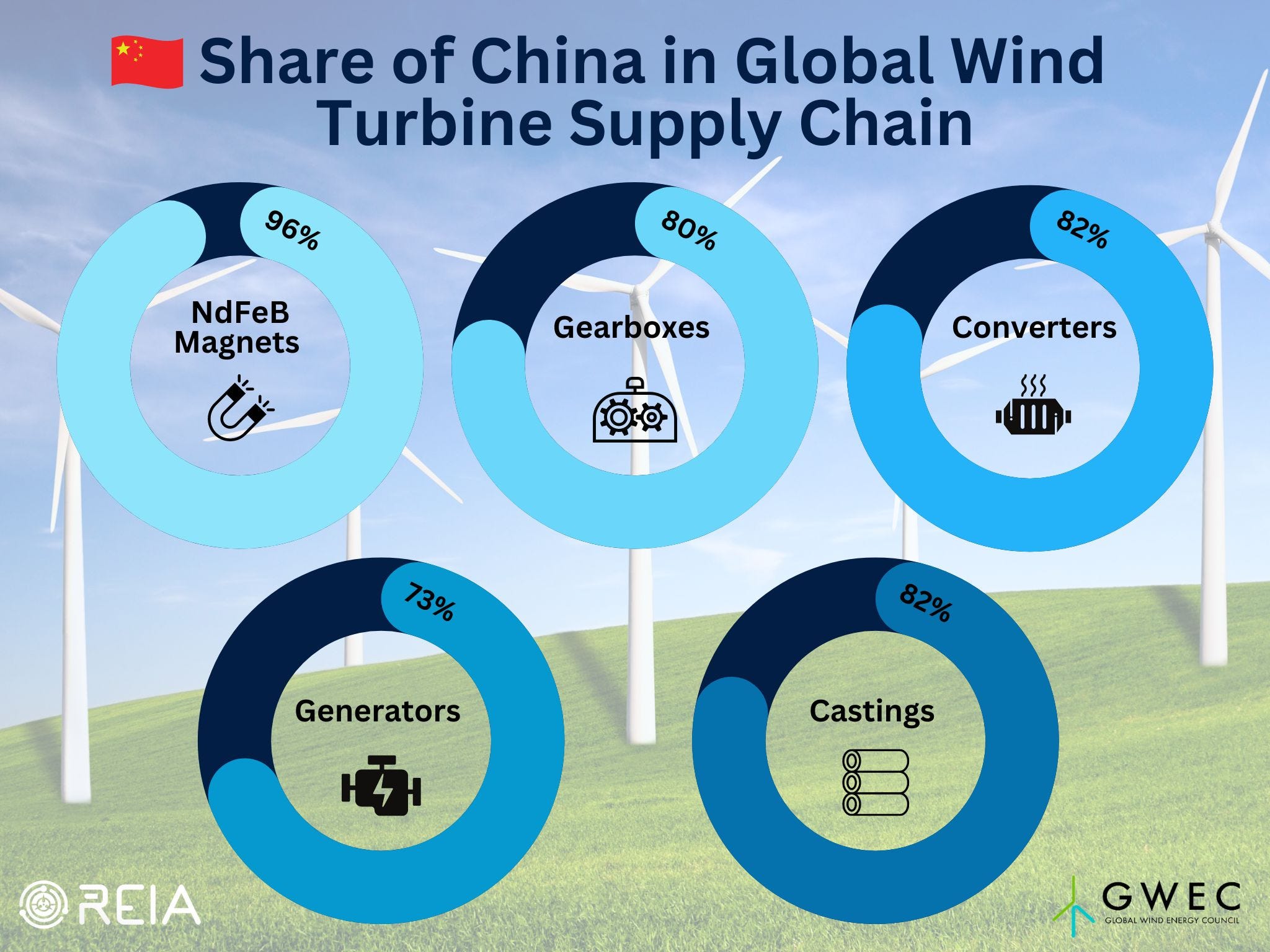

Pillar II: Wind Turbines

Wind turbines are the domain of China:

Major EU wind turbine manufacturer Vestas reduces its production of direct drive turbines, requiring a large volume of NdFeB magnets, in favour of a geared turbine, which requires a lower volume of NdFeB magnets.

Vestas expect to completely phase out rare earth permanent magnets by 2040.

And the largest EU market for wind turbines is…

Germany is currently also the EU’s largest markets for wind turbines with the highest growth forecasts. It was expected to grow substantially during 2023 and 2024. The German budget cut will have an negative impact on the roll-out of wind turbines as well.

Originally EUR12.6 billion spendings had been planned under the German Renewable Energy Act (EEG) for 2024. The target of the act is to increase the share of renewable energy to 80% of energy output.

In terms of wind turbine installations Germany had already been limping behind, and this budget cut won’t contribute to any improvement.

Rare earth relevance

China’s government is determined to retain its dominance of rare earths and rare earth permanent magnets, and to expand its presence in the international EV market to a level of domination as well.

This comes along with significant ongoing upstream capacity expansions in rare earth processing and increased production capacity of high performance rare earth permanent magnets. These expansions have been designed considering all factors and of course include the glowing consumption growth forecasts of analysts, which base on political targets/announcements of governments.

With its own home market for EV slowing, magnet and rare earth exports slowing, China must rely more on EV exports. Jan-Oct 2023 China’s EV exports are up 81% year on year at 1.3 million fully electric vehicles.

One third of China’s EV exports in Q1-Q13 2023 were headed for the EU. Within the EU Germany is the largest EV market, and, as described above, that one is stalling.

Going forward

During 2023 rare earth and rare earth permanent magnet demand was sluggish owing to China’s domestic economic situation. Particularly the real estate slump affects all other sectors of China’s economy.

And now it will be Germany, who is failing rare earths.

Rare earths: Supply up - demand flat

We see expanding Chinese supply of rare earths and rare earth permanent magnets meet a market that expands below expectation.

Unless the U.S. bail out the market by increasing magnet imports from China even beyond the +15% of the first three quarters 2023, we expect both principal growth pillars of rare earths and rare earth permanent magnets taking a hit in the year ahead.

In terms of rare earth prices in 2024 this does not bode well.

Unusual third batch of rare earth production quota

China’s Ministry of Industry & Information Technology just issued an unusual 3rd batch of rare earth quota to China Rare Earth Group and to China Northern, bringing up the total quota for the year to 255,000 tons TREO for mining and to 243,850 tons TREO for smelting and separation.

A year on year increase of 20%.

Add to this the TREO quantity from rare earth raw material imports, which are not subject to quota.

Keep reading with a 7-day free trial

Subscribe to The Rare Earth Observer to keep reading this post and get 7 days of free access to the full post archives.