Defense Hype; China Magnets ad nauseam; China RE Imports from Myanmar jump; Who is REalloys?; MP's CF; LCM: British invade France; Lynas Jr Miner Hype; Finally: Hastings settle with Wyloo; and the lot

Rare Earth 03 June 2025 #176

Note

A long sermon to put things into perspective. A lot of falsehood is out there, meandering through the (sponsored) media and spread by consultant foghorns.

U.S. tariffs

Off and on again.

Bloomberg reported:

A panel of three judges at the US Court of International Trade in Manhattan issued a unanimous ruling Wednesday which sided with Democratic-led states and small businesses that accused Trump of wrongfully invoking an emergency law to justify the bulk of his levies. The court gave the administration 10 days to “effectuate” its order, but didn’t spell out any steps it must take to unwind the tariffs.

The judges rejected the government’s argument that Trump had authority to unilaterally issue tariffs under a law intended to address financial transactions during national emergencies. The ruling was a so-called summary judgment, meaning a final victory for the plaintiffs in lower court without the need for a trial.

Anyway, rare earths had been on the tariff exemption list of the White House. And the bottleneck for rare earth permanent magnets is in China, not in the U.S.

What this does is showing impressively to the opposition on the other side of the Pacific Ocean what real rule of law can be.

Confused about applicable tariffs?

China Briefing tried to sort it out for the rest of us, pretty comprehensively:

Breaking Down the US-China Trade Tariffs: What’s in Effect Now?

China’s dual use licensing - some thoughts

China’s officialdom reasons that the 7 rare earth elements are subject to China’s dual use export licensing under China’s domestic rules & laws, as well as national interests, “and to fulfill international obligations such as non-proliferation”.

The international arms non-proliferation agreements that China signed you can find here. They are all about non-proliferation of ABC (atomic, bacteriological, chemical) weaponry, nothing about conventional weapons, as far as we can see.

In terms of “international obligations” emphasis of China seems to be the Treaty on Non-Proliferation of Nuclear Weapons (NPT) which China signed in 1968 .

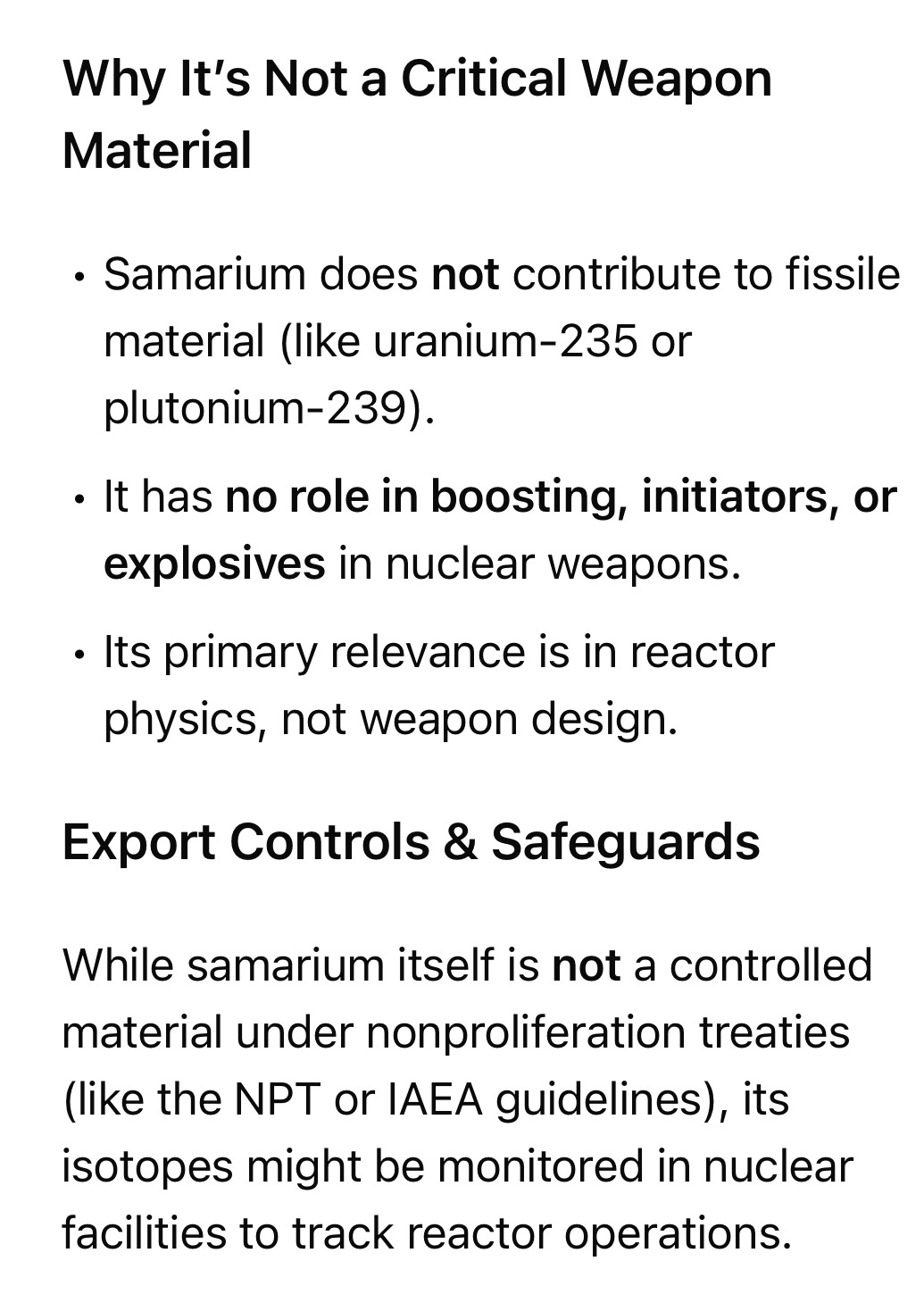

Have you ever asked yourself, what the actual use of any of these 7 elements (samarium, scandium, gadolinium, yttrium, terbium, dysprosium and lutetium) should be in terms of nuclear weapons?

Just one example: Samarium-149 is a stable isotope and a powerful neutron absorber, thereby inhibiting chain reactions and reducing energy yields. An undesirable for nuclear weapons, as per our layman research.

Answer from China

Dissatisfied with our research, we decided to ask the latest version of China’s very own, strictly government-controlled DeepSeek AI, whose product design and research has been located in Beijing’s Haidian District since 2023, not very far from China’s Ministry of State Security at Yidongyuan. Here DeepSeek’s conclusion for samarium:

We asked DeepSeek the same question for every single one of the remaining 6 elements.

The conclusion for all elements was in unison with the above, with the following exceptions:

Terbium and dysprosium alloys, and

Dysprosium-alloyed NdFeB magnets

may qualify for dual-use control, explicitly not under the NPT, but under the Wassenaar Arrangement on Export Controls for Conventional Arms and Dual-Use Good and Technologies, which includes conventional weapons and other defense-relevant equipment.

Non-membership detriment

China is not a member of the Wassenaar Arrangement, even though it tried to become one. The reason: China does not meet the Wassenaar Arrangement membership requirements.

Needless to say, China disputes its non-qualification and rather views the Wassenaar Arrangement as a tool to contain China.

Our take

Not being a member and contesting its purpose, China could not use the Wassenaar Arrangement as a base for dual-use licensing of whatever product.

The fact that several parties in the Myanmar civil war as well the Myanmar governing junta use Chinese weaponry and ammunition (which is a consumable and needs to be procured constantly) shows impressively, how effectively China’s arms-control works: not at all.

Also the M23, who wreaks havoc in the eastern part of DR Congo, allegedly uses China-made mortars, artillery and surface-to-air missiles.

China’s implied reference to the Treaty on the Non-Proliferation of Nuclear Weapons holds no water for the elements in question, unless common steel would be deemed dual-use, too. Only relying on domestic, perceived to be “rubber stamp” laws is a crucial weakness (actually, there are proposed laws in China that create controversy and are hotly debated. Many laws are not just waved-through by the National Peoples Congress Standing Committee).

Rare earth licensing in China

To make that absolutely clear, there is a lot of licensing involved in China’s rare earth. The minimum is:

Business license: Each company handling rare earth must have it explicitly mentioned in its business license.

Special invoice: Each company must only invoice rare earth on special rare earth invoices, different from the normal VAT invoices.

Export license: Every single export of rare earth is subject to a license from the Ministry of Commerce.

Dual-use license: Each export Samarium, scandium, gadolinium, yttrium, terbium, dysprosium and lutetium, or products containing more than 0.1% of any of these, must be licensed under the dual-use licensing system.

If a company has a dual-use export license, it does not need to apply the export license under (3). What a generous bureaucratic relief!

The license under (3) can’t be used to interfere in rare earth exports, as this would be WTO non-compliant, as proven already in 2014.

So, China’s bureaucrats needed to refer to a “dual-use” issue.

Defense hype

A usually well-informed source in China says, that the dysprosium content of an F-35 fighter jet should be quite precisely 417 gram, not only as an alloy of NdFeB but also as a part of a certain other alloy.

Another usually well informed source, this time from the West, puts the overall rare earth content of an F35 at 4.5 kgs.

This number would commensurate with so far very low numbers of overall NdFeB rare earth permanent magnet use in the U.S. military which we hear from western sources. Less than 200 t/y.

Why? Tiny quantities of rare earths have a huge impact.

The proposed rare earth military consumption numbers of junior rare earth miners and their sponsored foghorns are detached from reality.

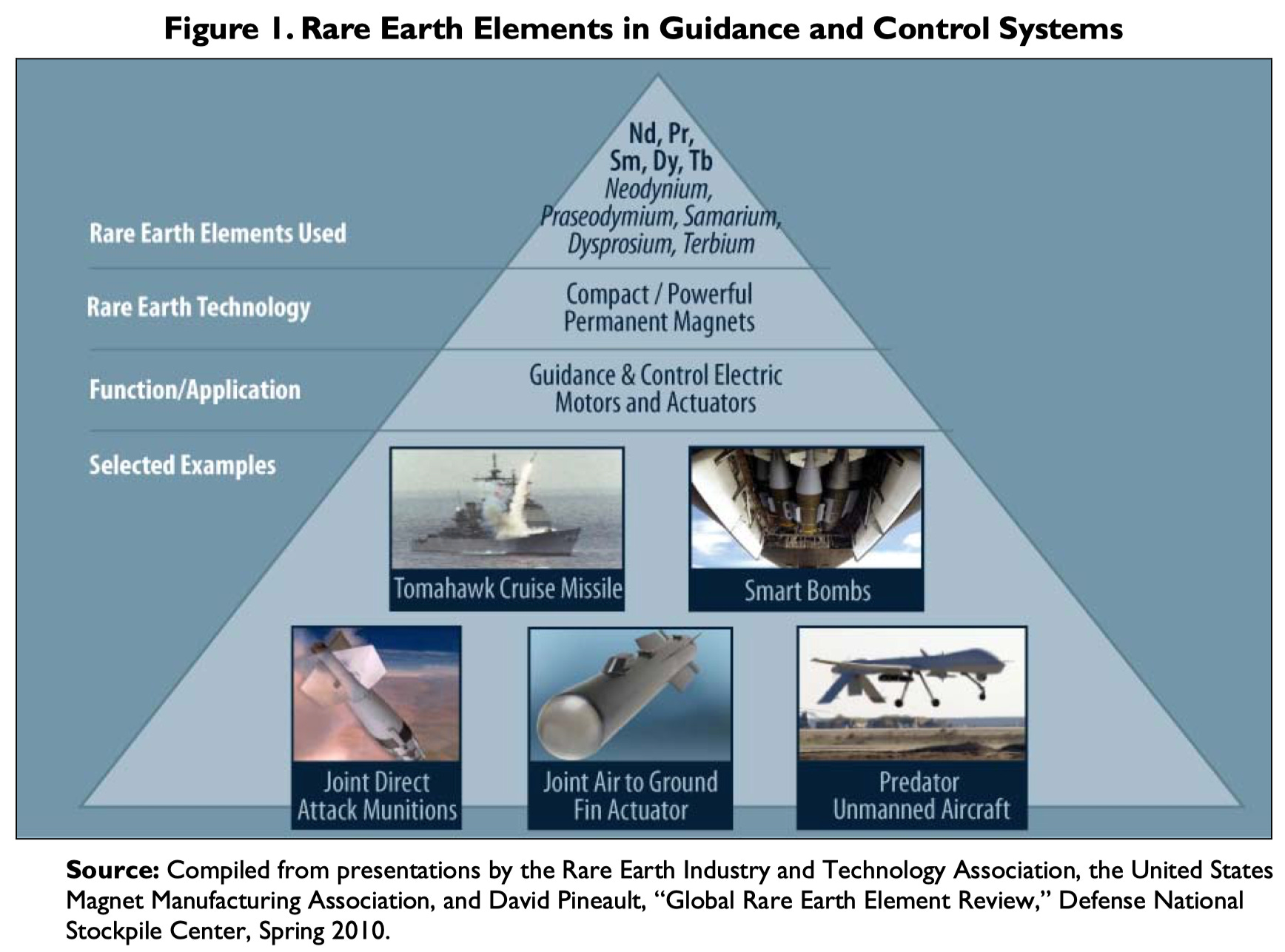

Default defense magnet: NOT NdFeB

We don’t get tired pointing out that the samarium-cobalt magnet is the default magnet in defense, owing to its high heat resistance, multiple times higher than the much hyped NdFeB magnet.

Where the working temperature requirement is lower, more powerful NdFeB magnets are used, for example in the actuators that control the fins of gravity-guided bombs.

Junior miners and their sponsored foghorns do not like that, because samarium is comparatively minor and boring for them.

Old story

You could have read it all 13 years ago in a U.S. Congress report of 11 April 2012:

It has been estimated that DOD uses less than 5% of domestic consumption of rare earths. 12 Rare earth elements are found in two types of commercially available, permanent magnet materials. They are samarium cobalt (SmCo), and neodymium iron boron (NdFeB). NdFeB magnets are considered the world’s strongest permanent magnets and are essential to many military weapons systems. SmCo retains its magnetic strength at elevated temperatures and is ideal for military technologies such as precision-guided missiles, smart bombs, and aircraft. The superior strength of NdFeB allows for the use of smaller and lighter magnets in defense weapon systems.

If these 5% should still be valid, then the U.S. defense purpose purchase of rare earths should have been less than US$10 mio in 2024.

The rare earth quantities required for each application are really small.

Tiny quantities - big impact

Basically, most of the things you can switch on and off in your household would not function, if it was not for often tiniest quantities of rare earths contained in each device, e.g. LED lighting.

Why would you even begin to think this should this be any different in defense?

That is, why rare earths are referred to as vitamins of industry. US$6 bio/year or so of rare earth driving up to US$10 trillion/year of global industrial output (based on one of the rare projections of Adamas Intelligence that we can actually agree to).

Scale

If defense demand for NdFeB magnets was as significant as junior miners and their sponsored foghorns want you to believe, why would the DoD settle for a factory that will turn out less than 2,000 t/y of NdFeB (eVAC), while in China 5,000, 10,000 and 20,000 t/y factories are built (with an eye on replacing many smaller factories, largely in the area of Ningbo)?

We agree with Jack Lifton, who repeatedly said that it is civil commercial demand that drives rare earth and rare earth permanent magnet consumption.

One NdFeB growth potential for U.S. military products is probably in drones for drone swarming, be it in aerial defense, battlefield killer drones, or in submarine tracking. But again, the rare earth magnets are so powerful, that - while the numbers may be large - their weight is disappointingly small.

US loudspeaker maker sounds the alarm on 'unnecessary' trade war

MISCO is just one example of the thousands of companies navigating the supply chain turmoil caused by U.S. President Donald Trump's tariffs on China and Beijing's countermeasures, including export controls on rare earths and the powerful magnets they create.

Amid the uncertainty, MISCO CEO Dan Digre has spent recent weeks in Southeast Asia trying to sort out the company's supply chain. He said he wants to make two things clear to the U.S. government: that tariffs are making it harder to build in America; and that there are no easy answers to sourcing magnets outside China.

"It's a fairly complex technology and a very specific technology," Digre told Nikkei Asia.

On the magnet front, MISCO is among the fortunate for now. China's dual-use export controls on seven rare earths have held up magnet supplies for many buyers, causing alarm among major users like automakers. The magnets MISCO uses contain no terbium and little dysprosium, and its suppliers said they were not caught up in the new licensing regime.

Related

China’s 2025 exports of Rare Earth Permanent Magnets

Total rare earth permanent magnet exports from China to the world (113 countries):

2024, Jan-Apr, destination world: 17,562,854 kgs, value $951,709,591

2025, Jan-Apr, destination world: 17,893,871 kgs, value $803,051,013

And, regarding the “special relationship” with the U.S., here China’s exports to USA during the first trimester:

2024, Jan-Apr, destination USA: 2,113,026 kgs, value $85,190,904

2025, Jan-Apr, destination USA: 2,202,400 kgs, value $110,446,803

So, then, all volumes up, what is everybody whining about?

This:

In April China’s rare earth permanent magnet export volumes to world were down 45% year on year:

2024, April only, destination world: 4,784,597 kgs, value $251,505,116

2025, April only, destination world: 2,626,734 kgs, value $114,888,040

The U.S. got special treatment, in April China’s rare earth permanent magnet export volumes to the U.S. were down 58% year on year:

2024 April only, destination USA: 594,053 kgs, value $28,123,955

2025 April only, destination USA: 246,329 kgs, value $9,980,020

And all that, while China’s magnet makers urgently need to fill under-used capacities. Fantastic!

American Chamber of Commerce in China: China's rare earth export restrictions showing signs of gradual easing

The Chinese government has gradually eased its rare earth export restrictions over the past week, according to the head of the American Chamber of Commerce in China. The Trump administration has expressed frustration that China has not moved forward with lifting export restrictions as promised.

Chamber representative Hart pointed out that "some approvals have been granted, though it is slower than the industry would like." "Some of the delays are because China is adapting to a new export approval system, not that they are not allowing exports."

China's rare earth strategic resilience has been underestimated; short-term confrontation is unrealistic

The Times of India published an article at the end of April this year, arguing that China's tightening of rare earth exports is not a good idea and will inadvertently weaken its dominant position in the global rare earth competition.

However, the author of this article believes that this view underestimates the strategic depth, investment scale and systematic layout that China has demonstrated in the past three decades to control key minerals. With decades of investment, technological advantages, professional talent training, supply chain integration and strategic acquisitions, China has established an unshakable dominant position in the rare earth field.

The article said that with the help of strategic industrial policies, China has established and funded a number of national rare earth laboratories, dozens of universities have opened specialized courses in key minerals and rare earths, and China University of Mining and Technology has topped the global ranking in the field of mining technology. Data shows that China has the most mining technology patents in the world.

“If the U.S. wants to address supply chain security issues through mineral diplomacy and build partnerships to replace sourcing from China, it must provide a certain level of financial or diplomatic support,” said Hou Lei, an associate researcher at the Institute of World Economics and Politics at the Chinese Academy of Social Sciences. “That’s why China’s irreplaceability will remain in the short term.”

The view from the other side of the Pacific Ocean.

After the U.S. has successfully tossed global trade into the bin, it should be mindful when it comes to global IP protection.

On the other hand, after having started to rid itself of global students, many of whom are traditionally at the core of U.S. R&D leadership, it seems the current U.S. strategy is anyway to exchange roles with China and assemble mobile phones in flyover states.

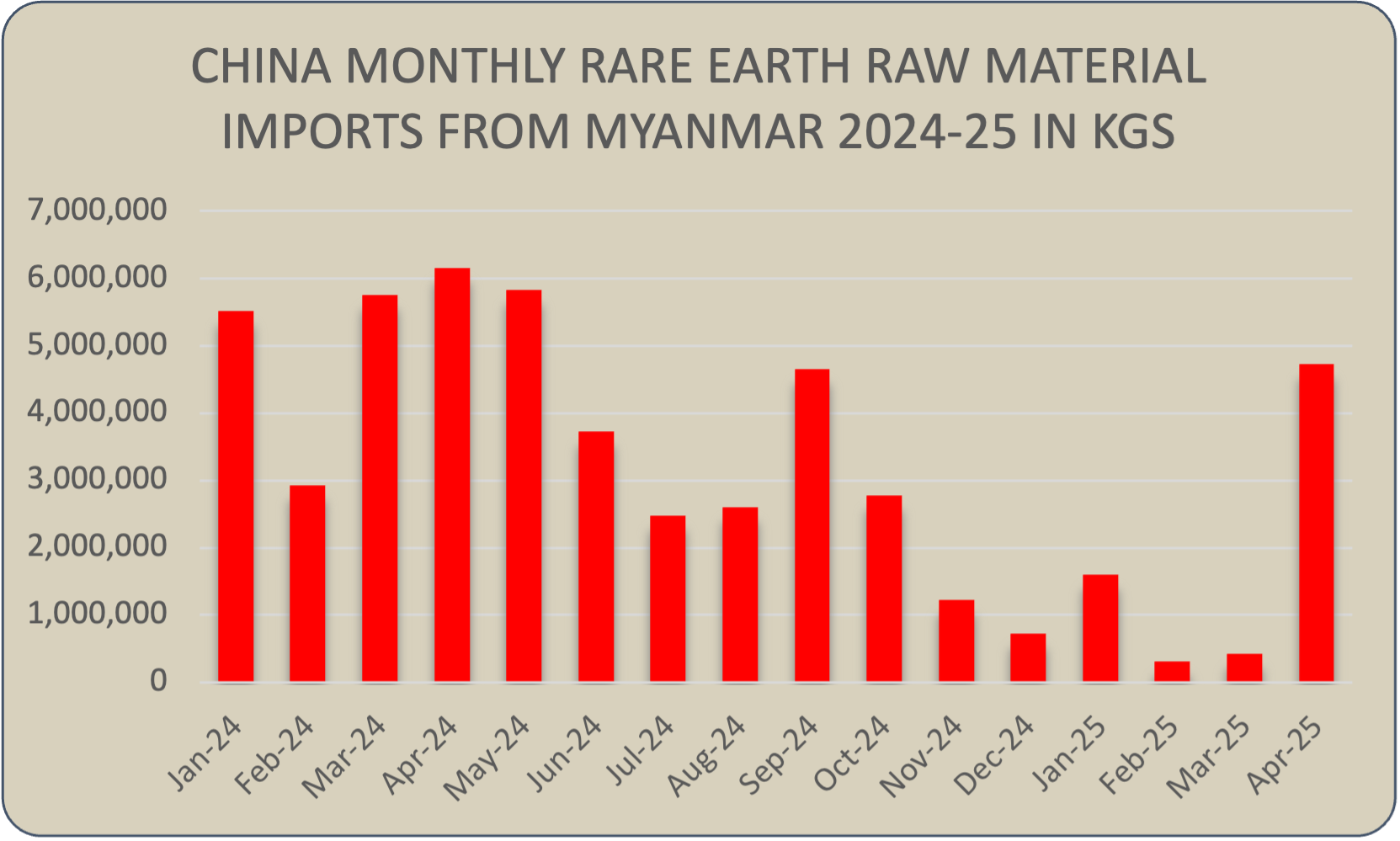

China’s Rare Earth Raw Material Imports from Myanmar jump in April

The average import price level is back to September 2024, before the Kachin Independence Army took control of the rare earth deposits in Myanmar.

It implies that China Rare Earth Group has settled with the Kachin Independence Army (KIA) and supplies of rare earth raw materials from Myanmar may go back to normal.

U.S. Pauses Exports of Jet Engine and Chip Technology to China

The Trump administration has suspended some sales to China of critical U.S. technologies, including those related to jet engines, semiconductors and certain chemicals. The move is a response to China’s recent restrictions on exports of critical minerals to the United States, a decision by Beijing that has threatened to cripple U.S. company supply chains, according to two people familiar with the matter.

Since their agreement to roll back tariffs in May, U.S. officials had expected the Chinese to relax restrictions they had imposed on critical minerals, but they do not appear to be pleased with China’s efforts.

Did the professionals in the current U.S. administration seriously expect that China’s commitment to multilateral, international agreements like the NPT would be for sale? Is this the thinking of a political elite who graduated from U.S. ivy-league universities?

As long as the U.S. accepts China’s reference to international agreements like the NPT in terms of dual-use rare earth export licensing, China retains the moral high ground. This line of reasoning needs to be obliterated.

The United States can always be relied upon to do the right thing — having first exhausted all possible alternatives.

U.S. Importer buys Chinese Rare Earth Permanent Magnet Equipment

An anonymous contributor pointed us to some interesting information.

We principally do not carry anything, that we can’t verify using publicly available information and resources.

The subject

Bonaventure International, a Delaware company, is on the record for having imported sintered NdFeB production equipment, instruments as well as Chinese NdFeB magnet blanks from several countries to the U.S.

Among others from these suppliers:

E-Heng Import & Export Co., Ltd. (上海易恒公司), China (a “fixer” for companies who are not licensed for the import and export of a certain item. This is a perfectly legal function used by many MNC in China for one-off imports or exports)

Baiqia Intelligent Technology (Ningbo) Co., Ltd. (百琪达智能科技(宁波)股份有限公司), China

Suzhou Yen Googol Electronics Co., Ltd. (苏州圆格电子有限公司), China

Dongguan Guorui Automation Equipment Technology Co., Ltd. (东莞市国锐自动化设备科技有限公司), China

Source: Dongguan Guorui Automation Technology Co., Ltd. website

Addresses

This is the building at 1700 S Pavilion Center Drive, Las Vegas, Nevada, a mailing address Bonaventure International use:

Among the tenants at 1700 S Pavilion Center Drive, Las Vegas, are:

Clark Hill International Law Firm

ER Injury Attorneys

Edelman Financial Engines

Howard Hughes Corporation

MP Materials

Northmarq Capital

PNC Bank

The Cirrus Company

Wynn Design & Development

The delivery address for some of the equipment and magnets Bonaventure International shipped from China was stated as 13840 Independence Parkway, Fort Worth, Texas:

Prohibited equipment?

According to China’s 2024 issue of the Catalogue of Technology Prohibited or Restricted for Export, NdFeB and SmCo technology export is prohibited.

If or not this should extend to the NdFeB and SmCo related equipment, may be subject to interpretation. However, rules & regulations in China are exclusively interpreted by the Chinese government and/or by the Chinese Communist Party on behalf of the government.

The particular equipment shipped from China to Bonaventure International, while necessary for NdFeB production, could perhaps be deemed non-core, potentially available also elsewhere on the planet.

As it appears, the company is not so benighted to procure all core NdFeB equipment from China, potentially illegal to export, which on top of that would need regular maintenance, spare parts and fine tuning by the Chinese manufacturer (never mind the manufacturer’s ‘kill-switch’ for expensive machinery).

SEC rules

If the company implicated by the choice of addresses should operate Bonaventure International, established 22 August 2024, while possibly not having disclosed it as a daughter company in violation of SEC rules, would be another topic.

Considering substantial public funding (=taxpayer money) offered to the implicated company, transparence and accountability should be paramount.

Seek truth from fact

A credit agency report, obtained by this humble blog, states about Bonaventure International:

The company does not disclose information about their shareholders.

It says that the operative address of Bonaventure International is at the above-mentioned 13840 Independence Parkway Fort Worth, TX 76177 and that no-one answered the phone there.

The agency attempted to conduct another interview:

We called MP Materials at (702) 844-6111 to ask if the companies are related but the person contacted hung up the phone.

Our take

If one had wanted to obscure the actual receiver and purpose of the equipment and magnet blanks shipped, then the chosen method is probably anywhere in-between unprofessional and plainly stupid.

We could not find any SEC filing that discloses Bonaventure International as an affiliate of MP Materials.

Also not in the latest Form 10-K, which under Note 19—Related-Party Transaction in terms of new information only carries the CEO’s private jet cost being paid for by loss-making MP Materials and the intended exit from the VREX minority joint venture with China.

Christian Morgenstern: That which must not, can not be.

Consequently, either a corporate construct may have been chosen that by the letters of the law and all applicable rules may qualify Bonaventure International as an unrelated third party, or it simply is a third party.

For example, it could also well be a daughter company of a contractor, using the customer’s addresses. There is precedence.

However, hanging up the phone when asked about Bonaventure International does not sound good.

Investors in Vietnam's renewables face jeopardy due to subsidies cut

More than 40 power project owners in Vietnam's wind and solar sectors have said they are at risk of defaulting and have called on the government to uphold the purchasing price at the favorable fixed rate previously agreed.

In recent years, Vietnam has promoted renewable energy by committing to purchase electricity at above-market prices for 20 years as part of a global shift towards cleaner energy sources. This move is also intended to address the country's growing electricity demand as its economy expands at one of the fastest rates in the world.

The favorable prices for solar projects range from 7.09-9.35 U.S cents per kWh, while authorities now want to pay investors in local currency at 1,184.9 dong (4.7 U.S. cents) per kWh. That represents a 34-50% drop in price based on the current exchange rate.

However, investors have experienced delayed or reduced payments from state-run Electricity Vietnam (EVN) pending a decision from top leaders on whether EVN will pay investors the price agreed in the original contracts. This was because of a government review stating that a construction completion acceptance (CCA) was missing from the project approval process.

The investors include Japan's Fujiwara Energy and Toho Gas, Thailand's B.Grimm Renewable, Super Energy and BG Energy Solution, Philippines' ACEN Vietnam Investment, Portugal's Sunseap Commercial Industrial Assets and Netherlands' SEP International.

Going forward, this does not bode well for domestic NdFeB demand in Vietnam.

Bloomberg

How Australia’s Luck Ran Out

Australia is pricing itself out of the market. Even nickel projects are not competitive anymore. The enormously expensive rare earth projects are the rule, not the exception. It is a general issue.

NSW mine reuse project - Summary report of site investigations

The NSW Mine Reuse project investigated the occurrence of critical metals in mining waste material. It involved a preliminary geochemical and mineralogical characterisation study across multiple metalliferous and coal sites on various waste material types, aiming to identify subsequent secondary prospectivity opportunities. The study was completed in collaboration between the Geological Survey of NSW, the Sustainable Minerals Institute at The University of Queensland, Geoscience Australia and RMIT University.

Downloadable reports and analysis data.

Very useful.

Nuclear Power Plants, Rare Earth Elements, and Horse Meat. A Conversation with the French Ambassador on Paris' Interests in Kazakhstan

Azattyk: During the visit of the President of Kazakhstan to Paris, cooperation between Kazakhstan and France in the field of rare earth elements was discussed. In May, you met with the Deputy Minister of Foreign Affairs of Kazakhstan and discussed this issue. What natural resources is France interested in?

Sylvain Guiguet: First of all, I want to say that we work on an institutional basis. Cooperation between France and Kazakhstan is one of the chapters of cooperation between the European Union and Kazakhstan.

In November last year, the governments of the two countries signed a roadmap in Paris, and its implementation has begun. The importance of rare earth metals is increasing due to technological changes. We are actively negotiating and soon, I hope, French companies will begin geological exploration on Kazakh soil.

Azattyk: Which French companies will engage in geological exploration?

Sylvain Guiguet: I cannot name the companies because the dialogue is at an early stage. But it is between France and the government of Kazakhstan.

Related

Karaganda geologists discover rare earth element deposit

During exploration work at the Kuirektykol site as part of the state program for geological exploration of the subsoil in the period 2022-2024, Tsentrgeolsemka LLC identified several promising areas with large resources of rare earth metals, which together amount to about a million tons.

The Kuirektykol site is located 300 km southeast of Astana, in the Karkaraly district of the Karaganda region, 100 km northeast of Karkaraly.

Geologically, the ore-bearing rocks of the Kuirektykol site are an ancient volcanic structure composed of extinct volcanoes and the products of their activity, which were subsequently altered by later magmatic processes.

In terms of mineralization scale, the most promising areas are the Irgiz and Dos 2 areas, where the content of the sum of rare earth elements exceeds 0.1%, reaching 0.25% and higher in individual samples.

A preliminary calculation of the reserves of the allocated block in the Irgiz area, carried out based on the results of core sampling and quantitative determination of rare earth elements, showed the presence of metals of about 800 thousand tons, with an average content of over 0.1%.

Azattyk Asia comments:

The news about the discovery of a large rare earth deposit with resources of 20 million tons in Central Kazakhstan may probably remind professional geologists of a bearded joke:

— Is it true that chess player Petrosyan won a thousand rubles in the lottery?

— True, but not the chess player Petrosyan, but the football player Akopyan, and not a thousand, but ten thousand, and not rubles, but dollars, and not in the lottery, but in cards, and did not win, but lost.

Maxim Klochkov, chief geologist of the company "Tsentrgeolsemka", which was engaged in exploration work in the Karaganda region, claims that there is no talk yet of any discovery of a deposit.

Safe to forget.

China’s Industrial Power Rates 2025: A Guide for Investors

Over the past few years, the average industrial power rate in China has increased slightly, reaching approximately US$0.088/kWh in 2024, up from US$0.084/kWh in 2019. Despite this uptick, China’s electricity prices remain lower than those in most developing countries, such as India and Mexico.

In 2025, China continued refining its power pricing mechanisms to improve cost transparency, promote efficient usage, and accelerate the integration of renewable energy. Notably, in the first quarter of 2025, China added 74.33 GW of new wind and solar capacity, bringing the total installed capacity of wind and solar to 1.482 billion kW, surpassing coal-fired power capacity (1.451 billion kW) for the first time. Beginning June 2025, all newly commissioned wind and solar projects are required to sell electricity through regional power markets rather than receive fixed feed-in tariffs. While this introduces pricing variability, it also enables qualified enterprises to pursue cost-saving opportunities via direct power purchase agreements (PPAs) and participation in the green electricity certificate (绿证) market.

EU average power price during second half of 2024: €0.1899 per kWh for non-household consumers with an annual consumption between 500-2,000 MWh. This was more than twice China’s price.

However, Sweden’s and Finland’s prices came close to China’s.

A good video to overcome outdated stereotypes.

Huawei-linked chip chemical supplier aims to replace Shin-Etsu, JSR, DuPont

Keep reading with a 7-day free trial

Subscribe to The Rare Earth Observer to keep reading this post and get 7 days of free access to the full post archives.