China tweaks RE Law Implementation; RE Price Moves demystified; Indonesia's & Morocco's RE Deposits; MP, Lynas, E-Tech, Energy Fuels, Lindian, Vital, CNRE.

Rare Earth 26 August 2025 #181

Note

More rare earth regulation from China?

SCMP says China was tightening rare earth rules. Of course media can’t be experts on everything they write about.

The Interim Measures for the Control and Administration of Total Amount of Rare Earth Mining and Smelting and Separation of 22 August 2025 regurgitate the contents of the Rare Earth Law and its implementation instructions with one significant difference.

Up do now the Ministry of Industry & Information Technology jointly with the Ministry of Natural Resources and the National Development & Reform Commission (whose function is better described under its previous name State Planning Commission) would issue the overall mining and separated rare earth production quota to the major rare earth enterprises and their respective provinces, who then would be in charge to subdivide the quota among their subordinated enterprises under the supposedly watchful eyes of the provincial government departments.

This apparently did not work.

According to this interim measure, the central government ministries take over the micro-management and assign quota on a per rare earth enterprise level, while continuing holding provincial governments responsible for the correct implementation.

All the rest, including the import raw material matter, was part of pre-existing rules & regulations, which The Rare Earth Observer featured exhaustively. But some professionals in rare earth don’t register until it appears as “news” in some mainstream media.

Ion-adsorption clay (IAC) rare earth in-situ leaching

Many junior rare earth miners bank on ion-adsorption clay in-situ leaching for recovering rare earth elements.

All of them advertise China-independence. Those exploring in Brazil are particularly loudmouth.

Has any of these rare earth hopefuls spent even a minute trying to figure out where the hundred thousands of tons of ammonium sulphate/bicarbonate required for their in-situ leaching should come from, other than from China?

Australia

We continue being negative on all mining plus processing investment in Australia, particularly rare earth. Amvest Terraden write:

The list of troubled metallurgical complexes is long. Glencore has approached authorities for support at its legendary Mount Isa copper smelter in Queensland, while Rio Tinto continues to warn of a challenging outlook for its Tomago aluminum smelter in New South Wales, the state’s largest power consumer. BHP has already suspended operations at its Western Australian nickel assets, putting them on ice a year ago. This has reduced supplies of sulfuric acid by-product, generating problems for the key rare earths producer in the region.

We repeat, Australia is trying to maintain a 1st world living standard based on a 3rd world concept.

Australians want to live like people in the EU, not like people in DR Congo and Indonesia. This increased and continues to increase the need to export ever more primary resources and leads OZ directly to the almost insane developments in Victoria, to sacrifice sustainable and productive farmland for unsustainable strip-mining of cheap minerals which have only one market to go to: China.

And now, having successfully reached global cost leadership from the wrong end while completely lacking a domestic market, Australians want to enter one of the most complicated, sophisticated and tedious value chains of all nonferrous metals, rare earths and subsidize a national reserve? Seriously?

Clickbait chasing

Media are chasing monthly trade statistics and turn every change into a clickbait-headline. Those with a bit of experience know that rare earths and rare earth permanent magnet exports from China have a history of monthly swings which are demand-driven and have nothing to do with export restrictions.

The negative effect of this year’s bureaucratic failures will equalise over time.

2011 Revival

The important take-home from the recent events is that China’s bureaucracy has turned China into an unreliable and unpredictable rare earths supplier. And that in spite of the promise of the chairman of China Northern Rare Earth Group at the Metal Events International Rare Earth Conference in Hong Kong 2018 that something like 2011 - the previous bureaucratic rare earth masterpiece - would never happen again.

This has nothing to do with the often private Chinese rare earth and permanent magnet suppliers. It has everything to do with China’s overconfident bureaucracy under a government that pursues projecting power proportional to China’s economic might, run by a party that has never given up on proselytism of two notorious German drunkards’ delusions, Marx and Engels.

There is of course no singular correct view of China, there are just too many angles and facets of what undoubtedly is a great nation. However, the Communist Party views the West and everything it stands for as a mortal threat to its own existence. It also has never given up the objective of world revolution, currently marketed as "Common Destiny for Mankind". Communists will continue to “struggle” against the West and its values, using all and any means.

NdFeB magnet alloys

There are still those who want to make the world believe that NdFeB magnets are one-fits-all commodities, that production is easy to emulate and involves only the proportional mixing and sintering of 4 rare earth elements. Lets walk through some examples of alloys, while remembering that the mortal enemies of NdFeB magnets are oxidation (rusting) and heat (mechanical, eddy currents):

Dysprosium and terbium: increase the coercivity and improve high-temperature stability. For every 0.1% increase in addition, the coercivity increases by approximately 20 kA/m. Magnets for wind turbines must contain up to 1.8% dysprosium to ensure flux loss below 3% at -40°C.

Gallium: addition of Ga can reduce the sintering temperature by approximately 30°C, reducing energy consumption while suppressing abnormal grain growth.

Niobium: Nb refines the grain size and improves mechanical strength.Addition of 0.5% of Nb to magnets for automotive use to improve vibration fatigue resistance.

Cobalt: MRI equipment requires a cobalt content of ≥2% to reduce eddy current losses.

Aluminum and copper: optimize the grain boundary structure and reduce the risk of intergranular corrosion.

Zirconium and molybdenum: Zr and Mo improve material density and surface finish by inhibiting oxidation reactions.

In order to prevent high magnet temperatures from eddy currents which degrade the magnet performance, the resistivity of the NdFeB magnet should be increased. As far as we understand, there is still no effective way to prepare magnets with both high resistivity and high performance.

However, rather than mechanical and chemical properties, magnets are defined by their physical properties. All this is not as easy as some people want you to believe.

The West is Red – MP Materials as an SOE

Upon hearing of the highly market distortive deal between the US industrial/military complex and MP Materials we had the wicked idea of asking Deep AI to create an image of the CEO wearing a Mao Suit. The responses were so hilarious and egregious that we dare not publish them here. He would probably be grievously offended if he wasn’t so busy laughing his way to the bank. The ones who should be offended are the US taxpayers that are being asked to subsidise the production of NdPr magnets, the vast bulk of which the US military do not need.

Coming only weeks after we highlighted the mining industry’s seeming love-in with the command economy, we now have the intrusion of the Five-Year Plan into the mining space and the conversion of a NYSE-listed company into an SOE. So, it is not surprising that we are left wondering how much the team around the US President actually know about Rare Earths and critical metals. Most will be long gone from the halls of power when these interventions into the private sphere come to grief and the cost thereof is left on the doorstep of the taxpayer.

The West is Red refers to a Chinese Cultural Revolution song glorifying Mao Zedong: 东方红 The East is Red. Actually, the song originates in the 1940s. It was written in the Communist refuge in Yan’an.

The taxpayer shoulders the bill for multiple US-government failures to address basic economic needs of the nation.

Trump weighs using $2 billion in CHIPS Act funding for critical minerals, sources say

The Trump administration is considering a plan to reallocate at least $2 billion from the CHIPS Act to fund critical minerals projects and boost Commerce Secretary Howard Lutnick's influence over the strategic sector, two sources familiar with the matter told Reuters.

The proposed move would take from funds already allocated by Congress for semiconductor research and chip factory construction, avoiding a fresh spending request as it seeks to reduce U.S. dependence on China for critical minerals used widely in the electronics and defense industries.

Already running out of funds?

Trump Administration Said to Discuss US Taking Stake in Intel

The Trump administration is in talks with Intel Corp. to have the US government take a stake in the beleaguered chipmaker, according to people familiar with the plan, in the latest sign of the White House’s willingness to blur the lines between state and industry.

From what budget would that be funded? Education?

Who was bought and by whom?

Western demand for Rare Earths, in material form, is de minimis.

That is some fancy Latin to fool journalists that you are not publicly dissing them :-)

It is therefore fitting that, absent any knowledge of their subject, and armed with righteous indignation at “What China just did.” or “What China didn’t do.” the journalist community will reach for the obligatory Wikipedia money shot.

There will follow a long meandering discussion about how the USA “used to be” the leader in global Rare Earths mining, separation, and downstream value-added.

This was a long time ago.

The story of Mountain Pass, the US Rare Earths mine in California will be told and retold with great emphasis on “What China did” to hamper its progress.

Throughout these diatribes, no mention will be made that the Chinese firm Shenghe Resources helped fund the mine restart when the US Department of Defense (DoD) was invited by the Administrators of that, the third bankruptcy, to help fund it.

This year, more than eight years later, the US Department of Defense decided to spend far more than it would have at the bankruptcy auction to buy a stake in the operating company, MP Materials, that now owns and operates Mountain Pass.

I know all of this because I was a shareholder in Molycorp, the forerunner of the new entity MP Materials, before, up to, and including the third bankruptcy.

A very long, very detailed post, absolutely worth reading. There are a couple of points we disagree with:

The ex-China market: While the so-called magnet materials Pr, Nd, Tb, Dy and Gd currently represent more than 90% of the rare earth oxide market value and 92% of this market is exclusively in China (an inconvenient truth consultants parading the “global rare earth market” try to hide from their audience), it does not make the remaining rare earth elements any less important. If there is one thing everyone should know, it is that only tiny quantities of rare earths enable 100% of the functionality of their respective applications.

This even applies rare earth permanent magnets: The 6,163 metric tons of NdFeB magnets the US imported in 2024 (USITC statistics) came as 324,905,753 pieces - in average barely 19 gram per piece.

The trouble is that the infinitely wise people talking about rare earths have never even heard of words like multi-layer ceramic capacitor. Data centers need a lot of these. And AI data centers even need ten times as many as a regular data centers do. Go figure which rare earth element it is. Hint: it is not neodymium.

Without rare earths not even the lights in your home would work. Hint: No, it is not neodymium either.

Export prices: The author compared China domestic prices to export prices and found some negative margins. This could constitute dumping, if there was a foreign competitor complaining. In the absence of such competitors there cannot be a regular anti-dumping procedure. Actually, most of the time published China market prices do not reflect the actual transaction prices. Domestic sales prices in private transactions can be substantially different from published prices. As substantially different as production cost are among Chinese rare earth enterprises. So no case here.

Absurd forecast growth rates: The rare earth permanent magnet market split in two. One half is commodity NdFeB magnets, which are nice-to-have in many applications, but they are not necessarily irreplaceable.

The growth for the other half, the high performance NdFeB for applications in electric vehicles and wind turbines, the most difficult and hi-tech, was what everyone had been inspired by.

Meanwhile it occurs even to recalcitrant German Greens that renewable energy alone doesn’t work for Germany. The German government plans defy the laws of physics, mathematical statistics and basic economics.

The left-leaning German Tagesspiegel reports:

Only about a third of the wind power capacity installed in the EU uses permanent magnet generators. Although these are more efficient in wind turbines and do not require more maintenance-intensive gearboxes, manufacturers have long avoided these turbine types due to supply and cost risks, according to industry sources.

Germany, one of the largest wind tower markets, stopped subsidising wind towers two years ago, while the German consumer continues paying for electricity that hasn’t been produced and for electricity that is exported at “negative prices”. The “Energiewende” itself has turned out to be unsustainable.

Meanwhile the current US administration is pushing the electric vehicle and wind turbines off a cliff. This and the recent supply problems caused by an overzealous Chinese bureaucracy (just like in 2011), users everywhere may be quietly reconsidering what alternative non-China dependent, non-rare-earth solutions are there.

The same German daily reports:

Even e-mobility can do without permanent magnets made of rare earths, as BMW demonstrates with its sixth-generation engines. Instead of permanent magnet synchronous motors (PSM), the automaker relies on a combination of separately excited synchronous motors (EESM) on the rear axle and asynchronous motors (ASM) on the front axle.

Although this has some disadvantages, BMW claims that this solution is superior in real-world driving conditions. This makes BMW independent of the ecologically problematic mining of rare earths and the high costs involved, and reduces the geopolitical problems that can affect the supply chain and thus production. Tesla also announced in 2023 that it would no longer use rare earth magnets, but has not provided any details since then.

The end of the high growth rates of high performance rare earth permanent magnet comes within sight, while the critical importance of rare earth elements in countless applications has not even been considered because of the mindless, increasingly insane magnet hype. In terms of rare earths a fundamental error.

Australia: the projects the author discusses are all dead in the water for lack of both, technical and economic feasibility. In terms of downstream investment Australia is a no-go zone.

Feasibility: All projects continue repeating the same conceptual errors, “mine to oxides” or “mine to magnets”. The finance periods will be too long and thereby working capital requirements will be much too high. It will suffocate them. The requirements of every part of the rare earth supply chain are actually different and require a different set of skills altogether. In the country of the Masters of Rare Earth it is a distributed value chain.

We agree with the author that the universal absence of even minimal rare earth competence is rather frustrating.

However, journalists and politicians must be generalists, it is a job requirement. That is why neither media nor politicians realise that they are being lied at all the time.

Regarding junior rare earth miners’ competence:

Would you expect an iron ore miner to be knowledgeable about high-precision cold-drawn welded steel tubes and the market for that? No?

Then why would you expect the equivalent from a junior rare earth miner?

Pakistan’s new tango with Trump has rare earths and promises for the holy land

Pakistan’s new strong man, Field Marshall Asim Munir has been on a mission to woo the new US administration. For now his charm offensive has been successful in the US with the Trump administration favoring Pakistan over India. While this will focus more on what has been announced, Trump’s belief that Pakistan can be a source of rare earths and oil, what the US administration has chosen to leave out of the US President’s briefing is how difficult or impossible will this extraction be in areas such are Balochistan, Waziristan and Khyber Pakhtunwa which are hostile for Pakistani forces, where the Chinese have all but given up and due to whose hostility and support the US had to leave Afghanistan. If the US President were to continue along the path he seems to have charted, he will bring the US back to the same neighborhoods that Joe Biden quickly abandoned citing the Doha accords Trump himself had signed.

There is bastnaesite in North Waziristan, the border area to Afghanistan. But why even think about it, when there is so much basnaesite in more hospitable locations elsewhere on the planet.

The potential deposits of rare earth earths the world over are well-known, as are the dud-deposits. Yet the current US administration is still running around like a chicken without a head, and all that with the attention span of a toddler.

Fascinating.

Hyping Greenland

Why are China and the US fighting over Greenland's rare earths? | 60 Minutes

Hilarious, the two guys with the facial expressions like I-did-not-have-sexual-relations-with-that-woman (US-President Bill Clinton, 1998).

“Non-Chinese” is patently false.

Total China shareholding in ETM should be at least 24.25%:

As of 14 August 2025 China-owned OCJ Investment (Australia) Pty Ltd own 17.02% of ETM’s voting shares.

As of 14 August 2025 Shenghe Resources continue holding 7.23% of the voting shares of ETM. Shenghe Resources is a state-controlled entity in China.

In August 2018 ETM - in its former incarnation “Greenland Minerals” - signed an MoU with Shenghe Resources covering the entire output of Kvanefjeld, incl. uranium. In case you want to dive into Greenland Minerals’ history, you can find the documentation on the ASX under GGG.

Issues

Notwithstanding commercial issues from the substandard, miserable recovery rate of Kvanefjeld’s rare earth carbonate , the EU’s EURARE project provided no evidence of successful separation of rare earth elements from the Kvanefjeld resource. There is reasonable doubt elsewhere, too, if the Kvanefjeld resource should be suitable for rare earth element separation.

While 60 Minutes keeps digging into the uranium content, if there was ever a basic rare earth concentrate produced at Kvanefjeld with a uranium by-product ETM’s problem would actually be the radioactive thorium content which forms the bulk of radioactive waste output - an estimated 90,000 t over the currently 37 years of estimated life of mine. A mountain of provenly harmful radioactive waste with nowhere to go in the West.

ETM’s 3rd-party-financed US$11 bio arbitration against Greenland and Denmark is going to take many more years, if not decades. So meanwhile ETM will need to find other substance to survive on.

“Largest rare earth resource in the world, good for hundreds of years”?

So far all of Greenland’s “massive rare earth resources” - mostly consisting of eudialyte and steenstrupine - have successfully resisted decades of attempts to separate rare earths from them.

At this point of time, if Greenland’s rare earth should be the answer, then it must have been a silly question.

Why China bothers

Hint: Shenghe Resources’ partner in China for the offtake of the Kvanefjeld resource was China National Nuclear Industry Corp (CNNI).

The EU Commission is still holding on to its illusions. For how much longer?

Northern Myanmar’s Rare Earths Are Shaping Local Power and Global Competition

Negotiations slowly gained momentum in December 2024 after a discreet meeting in Kunming, China, and the KIA began imposing a 20% levy on exported rare earth concentrates. By April, both sides agreed on a fixed rate of 35,000 yuan (USD 4,830) per metric ton. Trade resumed under KIA regulation, formalizing the non-state armed group’s de facto governance of a critical supply corridor.

This development is set against the backdrop of rapid growth in regional rare earth mining and exports. According to ISP-Myanmar, the approximately 130 active mining sites in northern Kachin State in 2020 rose to over 370 by the end of 2024. In Chipwi alone, more than 2,500 leaching pits have been recorded. Between 2017 and 2024, Myanmar exported over 290,000 tons of rare earth material to China, with a total value exceeding USD 4.2 billion, 85% of which was generated after the coup and about one third of which was generated in 2023.

The KIA’s seizure of Chipwi and Pangwa redefined the group’s strategic role: no longer solely a territorial insurgency, the KIA now governs key resource zones, manages export taxation, and negotiates directly with a major regional power, much like it did with jade mining revenues in the mid-1990s to entrench its autonomy and build administrative capacity .

The KIA model is beginning to resemble that of the United Wa State Army (UWSA), which has long controlled tin exports to China. The UWSA utilizes informal taxation, providing stable resource access in exchange for political non-interference. China may tolerate a similar form of armed commerce in Kachin.

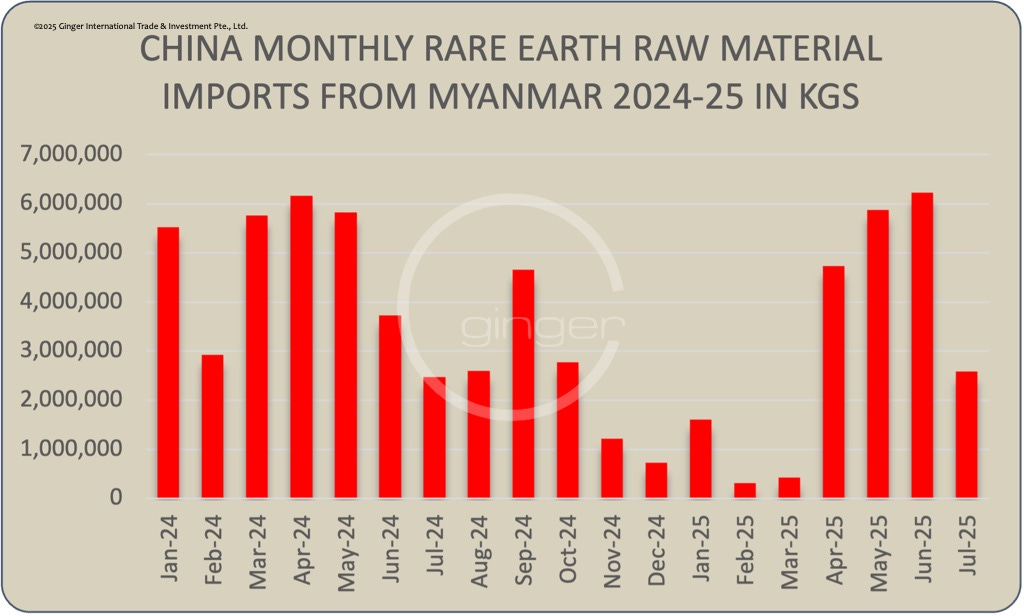

China’s import cost of rare earths from Myanmar in July were up, volumes were down:

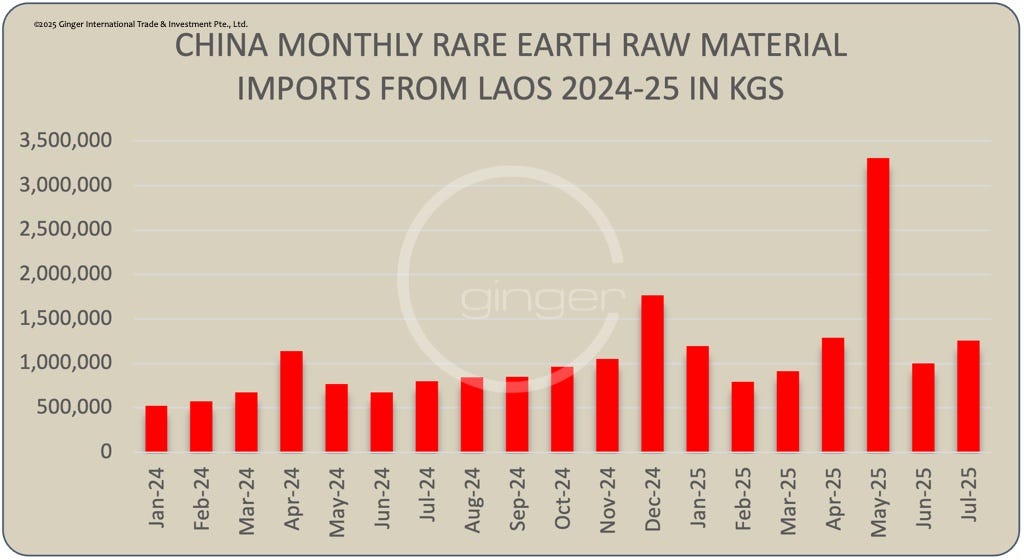

For good measure, here is Laos:

No clickbait here, it is only the market for heavy rare earth having been flat in Q2. Find the reason why in the Prices section.

Thais fear Myanmar rare-earth mining is polluting rivers

Things began to change early this year. The Kok River, which flows through the town, is usually crystal clear during the dry season, but this year the waters stayed muddy. When residents requested a water inspection, authorities found harmful heavy metals such as arsenic in excess of normal levels.

The Kok flows from Myanmar into the Mekong. The results at Mae Ai led authorities to expand testing to 27 sites along the Mekong and its other tributaries. More than half found unusually high amounts of arsenic, with some detecting nearly five times normal levels. In some places, authorities also found high amounts of manganese and lead.

Suspicion has turned to rare-earth mining in upstream Myanmar.

By May, nongovernmental group International Rivers used satellite imagery to identify at least 20 mining sites in northeastern Myanmar's Shan State, near the Thai border. Brown patches dotted the deep green mountains, showing mining wells and heavy machinery.

Thai authorities urge residents to avoid using the river water for drinking and washing, but Pianporn Deetes of International Rivers calls this "insufficient," noting that the Mekong flows through six countries including China, Myanmar, Laos and Thailand.

"No one wants to buy fish," said Buntham, a fisherman in Chiang Rai, describing how daily income plummeted to 50 baht ($1.55) from 200 baht. "I'm scared to eat fish that I don't know is safe, but to survive I have to eat what I don't sell."

Baring ammonia pollution this rather sounds like pollution from acid-mine-drainage. So the likely suspects could include gold, copper, lead, and zinc. Relevant deposits in and around Shan State are in the areas controlled by the Maoist United Wa State Army, currently China’s best friend forever in Myanmar.

The Mekong directly affects the livelihoods of ca. 70 million people. Indirectly it is many more.

Communist comrades in Laos and Vietnam will not be amused, if China’s Communists do not finally begin to develop some rudimentary form of international solidarity when it comes to cross-border environmental matters.

Keep reading with a 7-day free trial

Subscribe to The Rare Earth Observer to keep reading this post and get 7 days of free access to the full post archives.